1 Table of Contents

HOME and the Low-Income

Housing Tax Credit

Guidebook

1 Table of Contents

TABLE OF CONTENTS

HOME and the Low-Income Housing Tax Credit Guidebook ......................................... 1

Table of Contents ............................................................................................................................ 1

INTRODUCTION..................................................................................................................... 4

Purpose of this Guidebook ...................................................................................................... 4

Overview of the Programs ...................................................................................................... 4

Why Use HOME and LIHTC Together? ................................................................................ 5

Stakeholder Motivations ......................................................................................................... 5

Organization of this Guidebook .............................................................................................. 6

CHAPTER 1: CONDUCT THRESHOLD ELIGIBILITY REVIEW ............................... 18

1.1 Overview of the HOME Program ............................................................................... 18

1.2 Overview of the LIHTC Program ............................................................................... 24

1.3 Preliminary Review of Project Applications for HOME-LIHTC Projects................. 33

1.4 Other Project Eligibility Criteria ................................................................................ 35

1.5 The Project Timetable ................................................................................................ 36

CHAPTER 2: REVIEW FINANCIAL FEASIBILITY....................................................... 38

2.1 Overview of the Financial Feasibility Review ........................................................... 38

2.2 Assessing Developer Capacity ................................................................................... 40

2.3 Reviewing the Project’s Marketability ....................................................................... 42

2.4 Financial Review of HOME-LIHTC Projects ............................................................ 45

2.5 Financial Analyses ...................................................................................................... 46

2.6 Reviewing the Development Budget .......................................................................... 46

2.7 Assessing Sources and Uses ....................................................................................... 50

2.8 Reviewing the Operating Pro Forma .......................................................................... 55

Table of Contents 2

2.9 Determining the Amount of HOME Subsidy ............................................................. 65

2.10 Negotiating the Best Position for the PJ ................................................................. 75

ATTACHMENT 2-1: CAPITAL NEEDS: SAVING FOR A RAINY DAY....................... 81

ATTACHMENT 2-2: HOW TO DETERMINE THE MINIMUM NUMBER OF HOME-

ASSISTED UNITS IN A PROJECT .................................................................................... 84

ATTACHMENT 2-3: HOW TO DETERMINE THE HOME COST ALLOCATION ....... 87

CHAPTER 3: COMMIT TO PROJECT AND CONSTRUCT UNITS ............................ 91

3.1 Environmental Review ............................................................................................... 91

3.2 HOME Written Agreements and Legal Documents ................................................... 93

3.3 Property Standards .................................................................................................... 101

3.4 Inspections ................................................................................................................ 104

3.5 Close-Out and Completion ....................................................................................... 105

3.6 Summary of Federal Requirements .......................................................................... 105

CHAPTER 4: LEASE-UP AND PROJECT COMPLETION .......................................... 109

4.1 Income Targeting ...................................................................................................... 109

4.2 Income Determinations ............................................................................................. 112

4.3 Rents ......................................................................................................................... 113

4.4 Recruiting and Selecting Tenants ............................................................................. 116

4.5 Leases ....................................................................................................................... 118

4.6 Project Completion and Close Out ........................................................................... 120

CHAPTER 5: ENSURE LONG-TERM COMPLIANCE................................................. 122

5.1 Affordability/Compliance Period ............................................................................. 122

5.2 Ongoing Property Standards and Inspections ........................................................... 124

5.3 Rents ......................................................................................................................... 127

5.4 Tenant Income Eligibility ......................................................................................... 129

3 Table of Contents

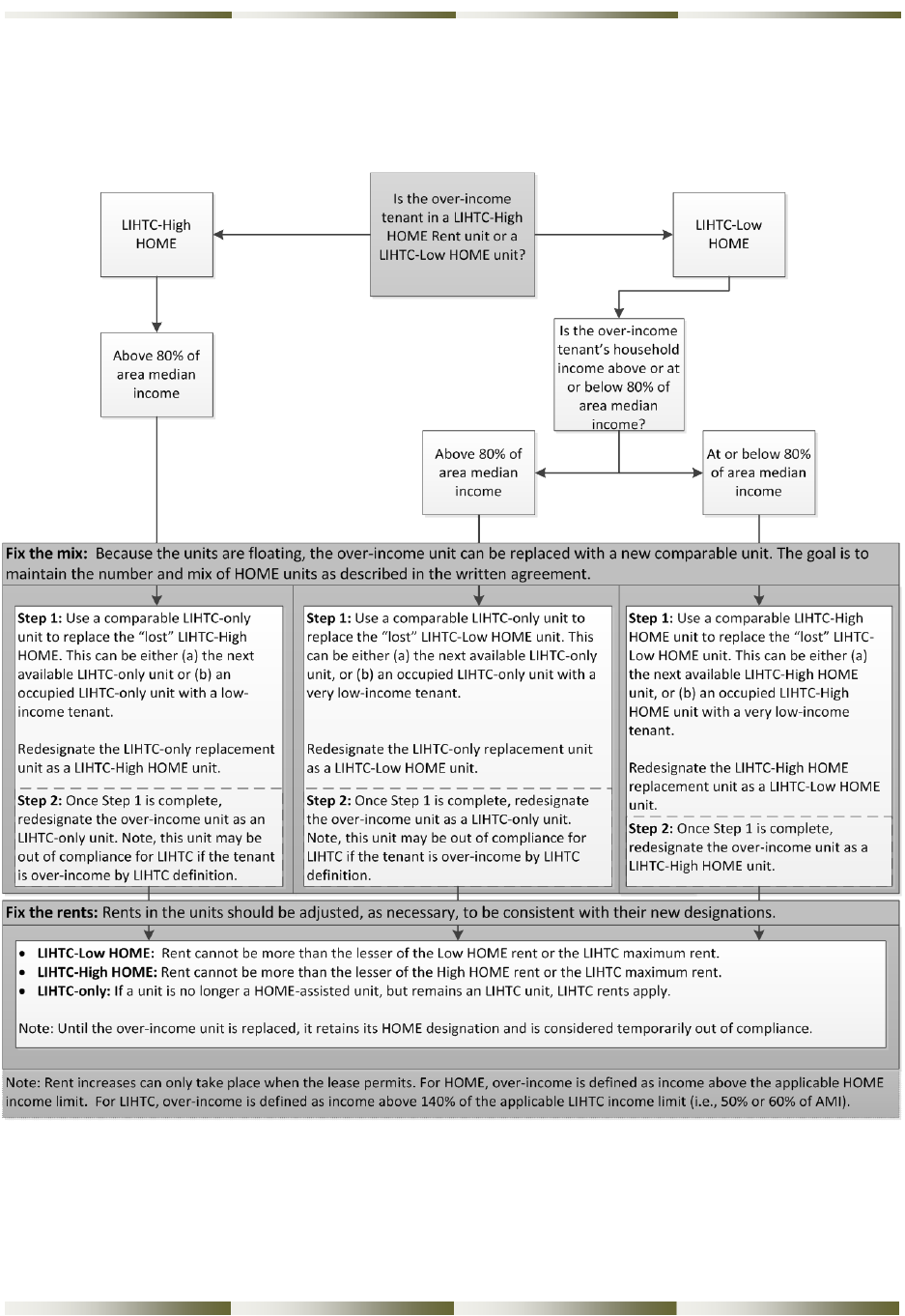

5.5 Maintaining Unit Mix ............................................................................................... 131

5.6 Terminating Leases or Tenancy ............................................................................... 149

5.7 Consequences of Noncompliance ............................................................................. 150

5.8 Early Intervention to Address Property Distress ...................................................... 152

CHAPTER 6: ADDRESS LONG-TERM AFFORDABILITY ........................................ 153

6.1 HOME and LIHTC Long-Term Affordability ......................................................... 153

6.2 Typical Investor Exit Strategies ............................................................................... 154

6.3 PJ Mechanisms to Preserve Affordability ................................................................ 156

6.4 Including Long-Term Affordability and Preservation of HOME Compliance into

Development Negotiations.................................................................................................. 160

Introduction 4

INTRODUCTION

Purpose of this Guidebook

When developers seek financial resources for affordable rental housing development, many

combine funds generated through the Low-Income Housing Tax Credit (LIHTC) offered by the

Internal Revenue Service with housing block grant funds provided through the HOME

Investment Partnerships (HOME) Program administered by the U.S. Department of Housing and

Urban Development (HUD). This publication, HOME and the Low-Income Housing Tax Credit

Guidebook, provides technical guidance to HOME Program Participating Jurisdictions (PJs) on

how to assess these HOME-LIHTC applications, and how to comply with the requirements of

both programs for the successful development of affordable multifamily rental projects.

While HUD has made every effort to describe the requirements of the Internal

Revenue Code accurately, HUD does not have oversight of the LIHTC. PJs

are cautioned that they must consult with legal and tax counsel or the Internal

Revenue Service when providing HOME funds to a project funded with LIHTC

to ensure that they understand the most accurate and up-to-date tax code

requirements. PJs should also contact their state’s Low-Income Housing Tax

Credit allocating agency.

Overview of the Programs

The HOME Program and LIHTC originate with different legislative histories and program

purposes. As such, each program has relative strengths and limitations in addressing a variety of

local housing conditions or needs.

The HOME Program was created in 1990 by the Cranston-Gonzalez National Affordable

Housing Act. Each year, Congress allocates approximately $2 billion by formula among the

states and hundreds of localities nationwide. HOME is the largest Federal block grant designed

exclusively to create affordable housing for low-income households in the nation. Among other

things, HOME funds may be used by PJs to provide incentives to develop rental housing through

acquisition, new construction, reconstruction, or rehabilitation of non-luxury housing.

Congress created the Low-Income Housing Tax Credit in 1986 as Section 42 of the Internal

Revenue Code (IRC or “the Code”) to develop a financial incentive to generate private capital

for the development of affordable rental housing. LIHTCs are administered by the Internal

Revenue Service (IRS) because they are tax credits, not direct funding, for affordable rental

housing development. Congress gives the states authority to allocate a certain number of tax

5 Introduction

credits to eligible affordable housing ventures annually. Therefore, while Section 42 of the IRC

regulates certain aspects of the LIHTC, each state also establishes certain priorities, policies, and

procedures for the allocation of its housing tax credits.

LIHTC is not the only Federal tax credit that can be used for affordable housing. The IRS also

offers tax credits for historic preservation (tax benefits to the project owner for maintaining the

historic character of a building) and energy (tax benefits to the project owner for making energy-

saving investments). In addition, several states offer their own low-income housing tax credits

and/or historic preservation tax credits, which serve as a credit against the investor’s state

income tax liabilities. This guidebook provides guidance only on the use of the Low-Income

Housing Tax Credit based on Section 42 of the IRC. It does not provide guidance on how to use

these other tax credit programs with HOME.

Why Use HOME and LIHTC Together?

HOME and LIHTC are often used together to finance affordable rental housing development. In

order to establish affordable rents in many markets, a project’s rents may not adequately support

sufficient conventional mortgage debt. The equity raised from the LIHTC may not be sufficient

to provide all of the additional capital required by the project. Often, HOME funds can be used

to finance the remaining gap.

Combining HOME and LIHTC funding also enables the developer and investors (including the

PJ) to:

• Leverage scarce resources

• Develop mixed-income housing

• Reach a diverse clientele (such as very low- and low- income residents) with the same

program activity.

When combining these two sources of funds, the projects must comply with the requirements of

both programs. Generally, this can be achieved by complying with the most restrictive

requirement. This guidebook illustrates how to do this.

Stakeholder Motivations

Generally, HOME PJs and LIHTC investors are not motivated by the same goals. The typical

LIHTC investor is motivated by its financial interests. Project and investment decisions are made

in the context of the tax implications and the financial impact on the investor. The investor

purchases a 99.9 percent interest in the ownership entity awarded LIHTCs for which it receives a

tax credit. This is a dollar-for-dollar credit against the investor’s tax liability for ten years, along

with other financial benefits generated by the project such as:

Introduction 6

• Operating losses resulting from the depreciation of the property

• Sharing of any net cash flow generated from the Net Operating Income of the project

• Benefits that may result when the investor exits the project.

PJs, on the other hand, are generally motivated by public policy objectives to provide affordable

housing to meet the needs of low-income families in their communities who are rent burdened or

living in substandard housing. PJs must be involved with the LIHTC project sponsors from the

beginning of the development process to ensure that their policy objectives are met, to ensure

long-term compliance with HOME affordability restrictions, and to negotiate the best return on

the HOME investment.

Organization of this Guidebook

The organization of this guidebook mirrors the development process for an affordable rental

project that uses HOME and LIHTC, from application and underwriting to project commitment

and construction to lease-up and ongoing compliance during rental property management. The

following chart describes these key HOME and LIHTC development steps and the associated

guidebook chapters.

Step 1: Conduct Threshold Eligibility Review. At this stage the PJ reviews the project

application for eligibility under HOME and LIHTC rules. This chapter covers topics

such as: an overview of the basic HOME and LIHTC program rules and roles,

coordination with the state tax credit allocating agency, eligible target population,

and eligible property types.

Step 2: Assess Financial Feasibility. Once the PJ is certain that the project is eligible, it

must assess whether the project is financially viable and likely to remain so over the

entire HOME affordability and LIHTC compliance periods. This chapter covers:

assessing developer capacity, assessing market risk, reviewing costs, reviewing

predicted operating expenses, and investing HOME and LIHTC funds.

Step 3: Commit to Project and Construct Units. After the PJ has decided to invest in a

HOME and LIHTC project, it must sign a written agreement with the developer and

manage the construction. This chapter covers: environmental review, written

agreements, deed restrictions, property standards, and inspections.

7 Introduction

Step 4: Lease Up and Complete Project. Once the construction is complete the PJ can

close-out the project and the owner can lease-up the units. This chapter covers:

income targeting and determinations, rents, leases, tenant selection, and project

completion procedures.

s

Step 5: Ensure Long-term Compliance. All HOME and LIHTC rental projects have an

affordability or compliance period during which the PJ must monitor for ongoing

regulatory compliance. This chapter covers: affordability period; ongoing property

quality; rent, income, and unit mix during the affordability period; and consequence

of noncompliance.

Step 6: Address Long-Term Affordability. At the end of the HOME affordability period

or the LIHTC compliance period, owners are free to convert units to non-affordable

uses. This chapter discusses steps that PJs may take to preserve affordable units.

As noted above, this guidebook discusses the HOME and LIHTC rules in the context of the

development process.

A glossary of key terms and concepts is provided as an attachment to this chapter. These terms

are identified throughout the guidebook in bold italics.

Introduction 8

GLOSSARY OF KEY TERMS

4 percent tax credits: 4 percent of the eligible basis is allowed as a tax credit per year for 10

years. 4 percent tax credits are available for existing housing or federally subsidized housing and

are generally used in conjunction with tax-exempt bond financing. 4 percent tax credits are also

referred to as 30 percent present value LIHTCs.

9 percent tax credits: 9 percent of the eligible basis is allowed as a tax credit per year for 10

years. 9 percent tax credits are also referred to as 70 percent present value LIHTCs. 9 percent

tax credits are available for new construction and rehabilitation.

Absorption rate: The number of units per week or month that is projected to be leased once the

property begins accepting residents. This number is expressed as a percentage of the total

number of units in the property.

Accessibility for persons with disabilities: The Fair Housing Act requires accessibility for newly

constructed housing. In properties with more than four units, the public and common areas, as

well as all the ground floor units, and units served by an elevator must meet the Fair Housing Act

accessibility guidelines. For people with sensory impairments, accessible also means that a

property makes reasonable accommodations to ensure their equal access and use. HOME-

assisted units are also required to meet the accessibility requirements of Section 504 of the

Rehabilitation Act of 1973, which for some projects, requires that a certain number of units be

made to be accessible in accordance with the Uniform Federal Accessibility Standards, for

persons with mobility and sensory impairments. Generally, UFAS is a higher level of

accessibility than the Fair Housing Act.

Affirmative marketing procedures: For properties of five or more HOME-assisted units, PJs

must develop marketing procedures to ensure that special outreach and advertising efforts are

made to communicate the availability of HOME-assisted units to those groups and individuals

least likely to apply for them.

Affordability period: The period of time during which a property must comply with the HOME

rules and regulations, including income and rent restrictions.

Applicable fraction: The share of the property that is LIHTC-assisted. It is based on the lesser of

either: (1) the number of tax credit units to the total number of units, or (2) the square footage of

the tax credit units to the total square footage of the property.

Basis boost percentage: Projects located in HUD-designated qualified census tracts or state

housing finance agency-designated difficult development areas can be allocated up to 30 percent

additional LIHTCs, at the discretion of the state LIHTC allocating agency. If the full 30 percent

addition is allocated, the basis boost percentage is 130 percent.

9 Introduction

Capital needs assessment: A projection of the likely timing and cost of replacement of building

systems (roofing, siding, mechanical systems, appliances, etc.) Often referred to as a CNA, the

analysis is expressed annually, over a 5-, 10- or 20-year period; it estimates the cost of

replacements in each year.

Capture rate: The share of renter households seeking housing of that type, in that location, and

at that price range, that need to be “captured” (i.e., leased) by the proposed property in order for

it to succeed. For example, a capture rate of 5 percent would indicate that 5 percent of the

potential, eligible renters in that market would need to become tenants.

Carryover Requirement: LIHTC projects must spend at least 10 percent of their projected total

basis as of the end of the second calendar year following the year of allocation. This is

sometimes referred to as the 10 percent test.

Cash flow waterfall: The priority ranking of the distribution of any surplus cash flow generated

by a multifamily rental property.

Community Housing Development Organization (CHDO): A private, nonprofit organization

that meets a series of qualifications prescribed in the HOME regulations at 24 CFR Part 92.2.

Comparable units: Under the HOME Program, units that are equivalent in terms of size,

amenities, and number of bedrooms. Units must be comparable in order to use them as

replacement units when maintaining unit mix. The LIHTC Program uses the concept of "next

available unit" for replacement units. LIHTC replacement units may be any unit in the same

building, as long as the LIHTC-eligible basis square footage is maintained.

Compliance period: See LIHTC compliance period.

Cost allocation: The process used to establish the allocation of costs and the minimum number

of HOME-assisted units in a HOME-assisted project, based on the amount of HOME investment.

Cost certification audit: Financial audits required by funders (including the state’s LIHTC

allocating agency) to certify actual project development costs. An initial audit may be used to

ensure that 10 percent of the project’s then-projected costs have been expended to meet the

carryover requirement. At the completion of the project a cost certification is required to confirm

the total development costs and the amount of LIHTC eligible basis in the project.

Debt service coverage ratio (DSCR): A calculation to determine the relationship between the

Net Operating Income (NOI) of a project to the amount of debt service the NOI must be used to

pay. To calculate DSCR divide Debt service (principal, interest, and credit enhancement

payments) by NOI. The DSCR is also referred to as “DSC,” or “cover.”

Introduction 10

Deed restriction or covenant: A legal document that restricts the use of a HOME-assisted

property during the affordability period for use as affordable housing for low- or very low-

income households as required at 24 CFR 92.252(e).

Deferred developer fee: The portion of the agreed-upon developer’s fee that the developer is not

paid as a development expense, and instead remains in the rental project to cover development

costs. The deferred developer fee may be recovered from the developer’s share of operating cash

flow.

Developer: A for-profit or nonprofit entity responsible for initiating and managing the

development of real estate, including the arrangement of financing, construction, and the

ownership structure.

Development budget: The cost estimate for all of the costs (or “uses”) that the developer will

incur to complete and lease-up or sell a project.

Direct investment: The simplest form of LIHTC investment in which a large corporation

purchases the entire investor interest in the project.

Eligible basis: In LIHTC developments, certain costs may be included in the calculation on

which the tax credits are based. These costs are referred to as “basis eligible” costs, and the total

of these costs is “eligible basis.” Eligible basis does not include land, financing fees, syndication

costs, or reserves, but does include the acquisition cost of existing buildings, construction and/or

rehabilitation, and most soft costs.

Environmental Assessment (EA): A concise public document required under the National

Environmental Policy Act (NEPA) regulations, for which a Federal agency (or an entity

authorized to assume HUD's environmental review responsibilities) is responsible that provides

sufficient evidence and analysis to determine whether to prepare an environmental impact

statement or issue a finding of no significant impact (FONSI). See 24 CFR 58.36 and HUD CPD

Notice 01-11.

Environmental Impact Statement (EIS): The environmental impact statement serves as an

action-forcing device to ensure that the policies and goals defined in NEPA are infused into the

ongoing programs and actions of the Federal Government. It provides full and fair discussion of

significant environmental impacts and informs decision makers and the public of the reasonable

alternatives which would avoid or minimize adverse impacts or enhance the quality of the human

environment. An EIS may be triggered as a result of an EA, but this is not common among tax

credit projects. See 24 CFR 58.37.

Environmental review: The appropriate level of environmental analysis for a project or activity.

This may include a Compliance Determination, Environmental Assessment, or Environmental

11 Introduction

Impact Statement. It is completed in accordance with 24 CFR Part 58 (known as a “Part 58

review”) to ensure that the proposed project does not negatively impact the surrounding

environment and that the property site itself is safe for development.

Exit strategy: An LIHTC investor’s plan for exiting their ownership position at the end of the

15-year tax credit compliance period.

Extended use period: In LIHTC projects, the period of affordability following the initial 15-year

period. (This is also referred to as the “LIHTC use period.”) All LIHTC projects must comply

with an initial use period of 15 years, during which time the investor limited partner must

maintain its ownership position. At the end of the initial 15-year period, there must be an

extended use period of an additional 15 years or longer (as required by the state allocating

agency) during which time the property continues to be restricted to affordable low-income

housing.

Fair Housing Act: See Federal Fair Housing Act.

Federal requirements: Broad Federal requirements that PJs must adhere to when administering

the HOME Program. These requirements include but are not limited to fair housing, lead-based

paint, Davis Bacon, accessibility standards, and the Uniform Relocation Act (URA).

Federal Fair Housing Act:

Title VIII of the Civil Rights Act of 1968 (Fair Housing Act), as

amended, prohibits discrimination in the sale, rental, and financing of dwellings, and in other

housing-related transactions, based on race, color, national origin, religion, sex, familial status

(including children under the age of 18 living with parents or legal custodians, pregnant women,

and people securing custody of children under the age of 18), and disability.

Financing gap: The shortfall in permanent financing sources that occurs when the total

projected development costs exceeds the total of all committed sources.

Fixed HOME units: Specific rental units that are designated as HOME-assisted initially, and

that retain the HOME-assisted designation throughout the HOME affordability period.

Floating HOME units: Rental units that are designated HOME-assisted initially but throughout

the period of affordability the designation is allowed to change or “float” among all comparable

units in the project in order to maintain the original unit mix of assisted and non-assisted units.

High HOME rent limits: The HUD-published High HOME rent limit. Current HOME rent

limits are available at http://www.hud.gov/homeprogram/

.

HOME written agreement: A legally binding document executed between the PJ and the owner

of a project that clearly states the HOME requirements, common expectations, roles and

responsibilities of the parties, and the PJ’s enforcement provisions.

Introduction 12

Housing and Economic Recovery Act (HERA): Effective July 30, 2008, HERA primarily

provides emergency assistance for the redevelopment of abandoned and foreclosed homes.

HERA also amends certain key LIHTC requirements and provisions.

HUD’s Office of Affordable Housing Programs (OAHP): The HUD Department that

administers three separate programs: the HOME Investment Partnerships, Self-Help

Homeownership (SHOP), and Homeownership Zone. These programs are designed to address

the nationwide shortage in affordable housing through the development of affordable housing

units and the provision of assistance to income-eligible households in the purchase,

rehabilitation, or rental of safe and decent housing.

Income recertification: The requirement that the owner/developer determine tenant incomes for

income-restricted units to ensure that such households’ incomes do not exceed the current

income limits. The income recertification requirements for HOME and LIHTC are slightly

different.

Income targeting: The process of designating units by the income of their occupants. These

requirements apply to the HOME- assisted and LIHTC-assisted units of a property.

Labor standards: The federally-regulated labor standards that apply to HOME-funded projects.

Davis-Bacon requirements apply to projects with 12 or more HOME-assisted units. Projects

funded solely by LIHTC are not subject to the labor standards.

Lead-based paint: Prior to 1978, lead-based paint was used in residential construction. Pre-1978

properties that are being rehabilitated using HOME and LIHTC must comply with the lead-based

paint regulations at 24 CFR Part 35 and meet the HUD Uniform Property Conditions Standards

(UPCS)

Lien position: The order of priority in which lenders’ claims and rights are recognized on a

property.

Limited liability corporations (LLCs): A legal ownership structure of two or more owners.

Typically one owner (known as a “member”) is designated as the “managing member” who

makes most day-to-day decisions. In an LIHTC project, the tax credit investor member(s)

typically is not involved in day-to-day decision-making, but is involved in major decisions such

as sales or refinancing.

Limited partnerships: A legal ownership structure similar to LLCs, except that the managing

owner is called the “general partner” and the investor(s) owner is called a “limited partner.”

Some limited partnerships have more than one general partner, in which case one of the general

partners is usually the managing general partner who makes most of the day-to-day decisions.

13 Introduction

Low HOME rent limits: The HUD-published Low HOME rent limit. Current HOME rent limits

are available at http://www.hud.gov/homeprogram/.

Low-income household: A household with a gross annual income that does not exceed 80

percent of area median income (AMI), as adjusted by household size. Current HOME income

limits are available at http://www.hud.gov/homeprogram/.

LIHTC basis: See Eligible basis.

LIHTC compliance period: The initial use period of 15 years, during which time the investor

limited partner must maintain its ownership position, and during which time the failure to

comply with certain LIHTC requirements may result in the cancellation or retroactive recapture

of allocated low-income housing tax credits.

LIHTC period: The 10-year period over which the investor may claim the LIHTCs. This is also

sometimes referred to as the “credit period.” This is not the same as the 15-year compliance

period.

LIHTC rent limits: The maximum rent that can be charged to tenants in an LIHTC-assisted unit.

It is limited to 30 percent of the applicable income limitation less utilities.

Market study: An analysis of a specific housing market to determine the demand for housing

units of a particular type and at a particular rent.

Maximum per unit subsidy limit: The upper limit restriction on the amount of HOME funds that

may be invested in a project; it is usually capped at the 221(d)(3) limit. These limits are

available at http://www.hud.gov/homeprogram/.

Mortgage (or a deed of trust in some states): The legal document executed between a lender and

an owner to subject a property to a claim or obligation.

National Affordable Housing Act of 1990: Title II of the Cranston-Gonzalez National

Affordable Housing Act (the HOME Investment Partnerships Act) which helps to expand the

supply of decent, affordable housing for low- and very low-income families by providing grants

to states and local governments called participating jurisdictions or "PJs.”

Net Operating Income (NOI): The amount of income remaining on a property after payment of

all operating expenses.

Net Syndication Price: The amount the investor pays for the low-income housing tax credits

that will be generated by the operation of the property. Price is expressed as an amount of one

dollar in credit allocation, so that an investor willing to buy $1 million of credits over ten years

for $750,000 is said to be paying $0.75 (seventy-five cents), or 75/100, or 75 percent.

Introduction 14

Net Syndication Proceeds: The total dollar amount that the LIHTC investor pays the LIHTC

project sponsor. It is based on the total project allocated credit amount multiplied by the net

syndication price.

Note: A written promise to pay a legal debt.

Onsite inspection: A physical inspection of a unit and/or property in order to determine that the

property complies with HOME and/or LIHTC property standard requirements.

Operating pro forma: A year-by-year projection of a project’s income and expenses.

Over-income tenant: A designation for a tenant when their household income exceeds the

income limits of the HOME and/or LIHTC programs. The definition of “over-income” differs

between the programs.

Owner: A for-profit or nonprofit entity that holds title to the property after rehabilitation,

construction, or acquisition.

Pari passu: Contribution of funds during development at an equal rate or pace, among all

funders. Pari passu is often relied upon in complex financial structures with more than one major

lender, to ensure that all funders have proportionately equal risk during construction.

Participating Jurisdiction (PJ): Any state, local government, or consortium that HUD has

designated to receive HOME funds and administer a HOME program. HUD designation as a PJ

occurs if a state or local government meets the funding thresholds, notifies HUD that it intends to

participate in the program, and has a HUD-approved Consolidated Plan.

Payment priority: The sequence in which payments of net cash flow from the operations of a

property are made to lenders, investors, and owners. See also “cash flow waterfall.”

Placed in service: Also referred to as the “placed in service date” or “PISD.” Placement in

service occurs when the first unit in an LIHTC building is certified as suitable for occupancy

under state or local law. Placement in service requirements differ for newly constructed and

rehabilitated buildings, and dictate the beginning of the compliance period in an LIHTC project.

Projects must be placed in service by the end of the second calendar year following the year of

allocation.

Program income: Gross income received by the PJ, state recipient, or a subrecipient directly

generated from the use of HOME funds or matching contributions.

Program Rule: At initial occupancy, 90 percent of the households served across all of the PJ’s

HOME-assisted rental programs must have annual gross incomes that are at or below 60 percent

of area median income. For each project, the PJ needs to determine how this rule applies. Many

15 Introduction

PJs restrict initial occupancy of High HOME Rent units to tenants that have annual gross

incomes that do not exceed 60 percent of area median income.

Project control: The entity with decision-making authority for the project.

Project Rule: At initial occupancy and throughout the period of affordability, in projects with

five or more HOME-assisted units, 20 percent of the households that occupy HOME-assisted

units must be very low-income (that is, have annual gross incomes that are at or below 50

percent of area median income) and be charged rents that do not exceed the applicable low-

HOME rent.

Property standards: Both the HOME and LIHTC programs require that units be constructed,

rehabilitated, and maintained to meet specified physical standards. The standard requirements

differ slightly for the two programs.

Qualified Allocation Plan (QAP): The annual plan developed by each state allocating agency to

document how it plans to make tax credits and tax-exempt bond financing available to

developers.

Qualified basis: The result of multiplying the amount of Eligible Basis (total tax credit eligible

costs) by the Applicable Fraction (the percentage of the property actually restricted to income-

qualified households). In LIHTC properties, the qualified basis is the amount used for

determining the credits that will be generated by the property.

Reservation (of credits): The notification from the state’s LIHTC allocating agency that a rental

project has been approved for an allocation of credits, and that those credits will be held for the

project pending construction and other requirements.

Reserves for Replacement: Funds held in a property’s restricted account to pay for its future

capital replacement needs. The term may apply to the amount held in the restricted account, or

the amount required to be periodically deposited to that account from the operations of the

property.

Right of First Refusal: The right to purchase a limited partners’ interest in a property, which

supersedes the rights of other potential purchasers.

Section 42 of the Internal Revenue Code (IRC or “the Code”): The section of the Internal

Revenue Code that regulates the LIHTC.

Sources and uses statement: A financial statement that projects and itemizes all of the uses of

funds needed to complete a project (development costs) and all of the sources of funds available

to cover those costs.

Introduction 16

Source documentation: Third party verification of income provided by independent sources that

is used to verify/determine tenant income-eligibility.

Sponsors: Under HOME, a for-profit or nonprofit entity that works with other organizations—

such as other nonprofits—to assist them to develop and own housing. At project completion, the

sponsor turns over title to the property to the sponsored organization. Under LIHTC, developers

are referred to as “project sponsors.”

Subordinate: To place below the rights of another set of requirements.

Subrecipient: A public agency or nonprofit organization selected by a PJ to administer all or a

portion of its HOME program.

Subsidy layering analysis: A financial review conducted by PJs when HOME funds are used

with other public funds in a project. It is done to verify that the project meets the underwriting

and cost guidelines established by the PJ and to ensure that no more HOME funds are invested

than are necessary to develop the housing.

Surplus cash: Cash that is not needed to meet operational requirements.

Syndicated transaction: The investor interest purchased by a fund or investor pool composed of

many corporations.

Syndication Fees: A fee the owner of an LIHTC project pays a syndicator to serve as a broker

between the equity investor and the developer.

Syndicator: An entity who arranges the housing credit investment, and represents the investors’

interests in the terms of the financial and legal structure of the investment.

Technical Guide for Determining Income and Allowances for the HOME Program: A HUD

guidebook in its Third Edition (HUD 1780-CPD, issued January 2005) that provides instructions

and forms to determine tenant income for the HOME Program. This guide is available at no cost

from the HOME Program website at http://www.hud.gov/homeprogram/.

Temporarily out of compliance: A situation in which an assisted unit is otherwise in

compliance with the provisions of the HOME regulations and written agreement except that

increases in the household’s income have exceeded the allowable limit, and a replacement

income-restricted unit has not become available. In the HOME and LIHTC programs, the

definition of “over-income” differs.

Threshold review: Preliminary screening of a project to ensure it meets all of the HOME and/or

LIHTC eligibility requirements.

17 Introduction

Total development cost: The total development cost (projected or actual), representing all costs

necessary to produce a completed, occupied project.

Total LIHTCs: This is the total dollar value of LIHTCs that the owner is expected to receive

over the ten-year credit period. It is based on the project’s qualified basis multiplied by the

applicable LIHTC percentage multiplied by ten years.

UFAS standard: The Uniform Federal Accessibility Standards are Federal accessibility design

requirements that apply to facilities that are designed, built, or altered with Federal funds.

Section 504 of the Rehabilitation Act of 1973 imposes the UFAS standard on certain HOME-

assisted units.

Unit mix: The range of unit types, sizes, rent, and occupancy restrictions of all rental units at a

property.

Utility allowances: In both the HOME and LIHTC programs, the maximum rent amount

allowed in both programs includes utilities. In projects where the tenants pay for some or all of

the utilities, a utility allowance is deducted from the rent limits to determine the maximum lease

rent that can be charged for the unit. LIHTC and HOME may use different utility allowances.

The PJ can choose to adopt the LIHTC utility allowance for its tax credit projects, to simplify

this process.

Very low-income household: A household with an annual gross income that does not exceed 50

percent of the area median income, as adjusted by household size.

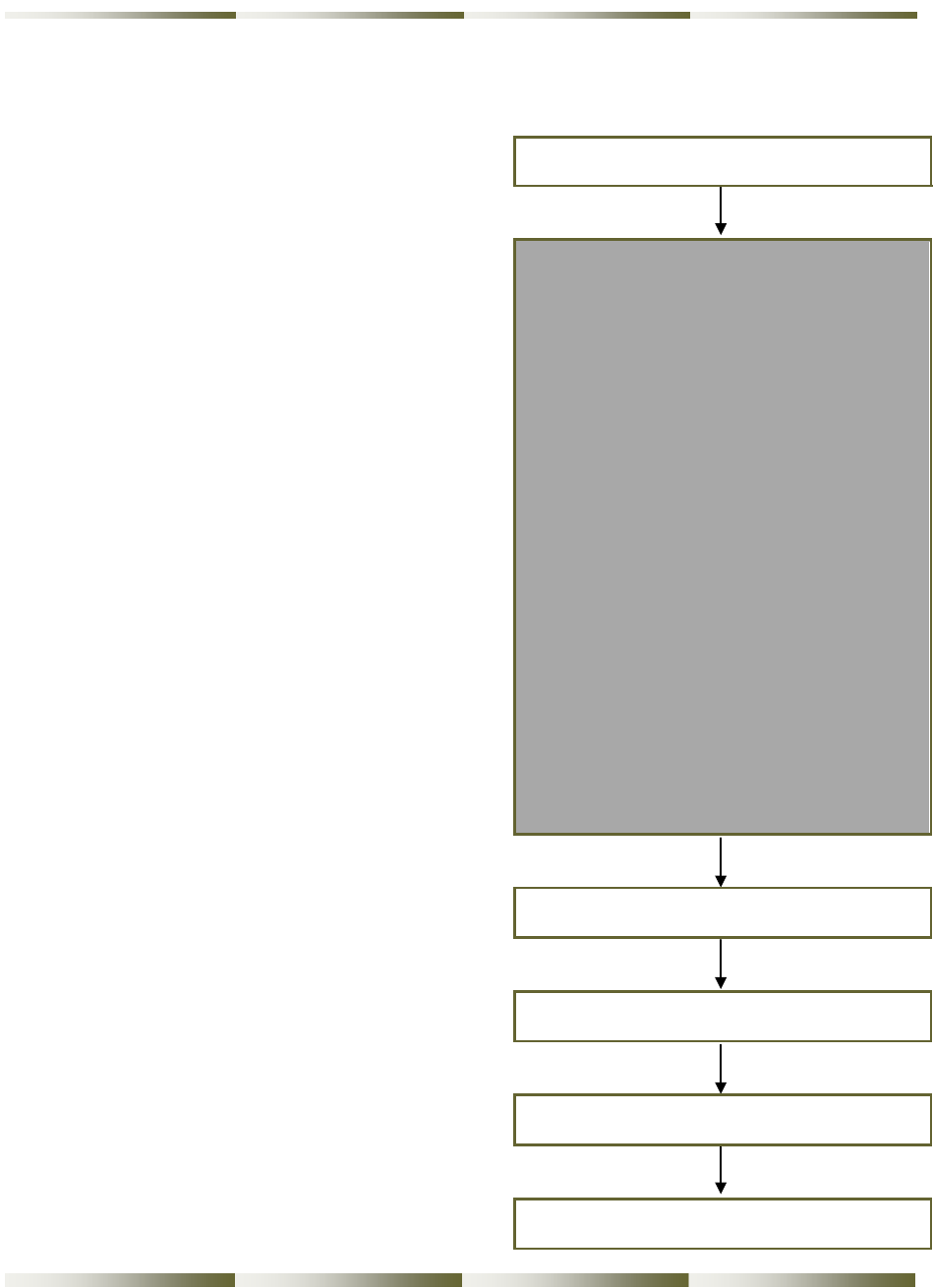

Chapter 1: Conduct Threshold Eligibility Review 18

CHAPTER 1: CONDUCT THRESHOLD ELIGIBILITY

REVIEW

This chapter describes the initial steps the HOME

Participating Jurisdiction (PJ) should take when it

receives a request for HOME funding for a project

that has (or expects to have) an allocation of Federal

Low-Income Housing Tax Credits (LIHTCs). It

highlights the key areas that a PJ should assess

when undertaking a basic eligibility threshold

review before proceeding to underwrite the project.

Specifically, this chapter:

• Explains the general HOME Program rules

• Explains, in general terms, how the LIHTC

program works

• Identifies the key eligibility criteria for a

HOME-LIHTC project.

1.1 Overview of the HOME Program

Created by the National Affordable Housing Act of

1990 (NAHA), HOME is the largest Federal block

grant available to communities to create affordable

housing. The intent of the HOME Program is to:

• Increase the supply of decent, affordable

housing to low- and very low-income

households

• Expand the capacity of nonprofit housing

providers

• Strengthen the ability of state and local governments to provide housing

• Leverage private sector participation.

CHAPTER 1: CONDUCT THRESHOLD AND

ELIGIBILITY REVIEW

1.1 Overview of the HOME

Program

Page 18

1.2 Overview of the LIHTC

Program

Page 24

1.3 Preliminary Review of Project

Applications for HOME-LIHTC

Projects

Page 33

1.4 Other Project Eligibility

Criteria

Page 35

1.5 The Project Timetable

Page 36

CHAPTER 2: REVIEW FINANCIAL

FEASABILITY

CHAPTER 3: COMMIT TO PROJECT AND

CONSTRUCT UNITS

CHAPTER 4: LEASE UP AND COMPLETE

PROJECT

CHAPTER 5: ENSURE LONG-TERM

COMPLIANCE

CHAPTER 6: ADDRESS LONG-TERM

AFFORDABILITY

19 Chapter 1: Conduct Threshold Eligibility Review

Every year, the U.S. Department of Housing and Urban Development (HUD) determines the

amount of HOME funds that states and local governments — the PJs — are eligible to receive

using a formula designed to reflect relative housing need. The HOME regulations may be found

on HUD’s Office of Affordable Housing Programs website at

http://www.hud.gov/homeprogram/, and in the Code of Federal Regulations at 24 CFR Part 92.

HOME Program Partners

To ensure success in providing affordable housing opportunities, the HOME Program requires

PJs to establish new partnerships and maintain existing partnerships. Partners play different roles

at different times, depending upon the project or activity being undertaken with HOME funds.

Key program partners include:

• Participating Jurisdiction. A Participating Jurisdiction (PJ) is any state, local government,

or consortium that has been designated by HUD to administer a HOME program.

• Community Housing Development Organization. A community housing development

organization (CHDO) is a private, nonprofit organization that meets a series of qualifications

prescribed in the HOME regulations at 24 CFR 92.2. Each PJ must use a minimum of 15

percent of its annual allocation for housing that is owned, developed, or sponsored by

CHDOs. PJs evaluate organizations’ qualifications and designate them as CHDOs.

• Subrecipient. A subrecipient is a public agency or nonprofit organization selected by a PJ to

administer all or a portion of its HOME program.

• Developers, owners, and sponsors. Developers, owners, and sponsors of housing

developed with HOME funds may be for-profit or nonprofit entities. Developers are the

entities responsible for putting the housing deal together. Owners are the entities that hold

title to the property after rehabilitation, construction, or acquisition. Sponsors work with

other organizations—such as other nonprofits—to assist them to develop and own housing.

At project completion, sponsors turn over title to the property to the other organization.

• Private lenders. Most HOME projects leverage or involve other financing, from for-profit

lenders or other entities such as foundations or community groups.

• Third-party contractors. Third-party contractors include a range of other entities that might

work on the HOME program, such as architects, planners, construction managers, real estate

agents, or consultants.

Chapter 1: Conduct Threshold Eligibility Review 20

HOME-Eligible Program Activities

HOME funds can be used to support four general affordable, non-luxury housing activities:

• Homeowner Rehabilitation. HOME funds may be used to assist existing owner-occupants

with the repair, rehabilitation, or reconstruction of their homes.

• Homebuyer activities. PJs may finance the acquisition and/or rehabilitation, or new

construction of homes for homebuyers.

• Rental housing. Affordable rental housing may be acquired and/or rehabilitated, or

constructed.

• Tenant-based rental assistance (TBRA). Financial assistance for rent, security deposits,

and, under certain conditions, utility deposits may be provided to tenants. Assistance for

utility deposits may only be provided in conjunction with a TBRA security deposit or

monthly rental assistance program.

Prohibited Activities and Costs

HOME funds may not be used to support the following activities and costs:

• Project reserve accounts. HOME funds may not be used to provide project reserve accounts

(except for initial operating deficit reserves) or to pay for operating subsidies.

• Tenant-based rental assistance for certain purposes. HOME funds may not be used for

certain mandated existing Housing Choice Voucher Program (formerly known as Section 8)

uses, such as Housing Choice Voucher rent subsidies for troubled HUD-insured projects.

• Match for other Federal programs. HOME funds may not be used as the “nonfederal”

match for other Federal programs except to match McKinney Act funds.

• Development, operations, or modernization of public housing. HOME funds cannot be

used alone or in conjunction with HUD-funded public housing program funds (e.g., Public

Housing capital programs such as Development, Comprehensive Improvements Assistance

Program (CIAP), or Comprehensive Grant Program (CGP)) to acquire, rehabilitate, or

construct public housing units.

• Double-dipping. During the first year after project completion, the PJ may commit

additional funds to a project. After the first year, no additional HOME funds may be

provided to a HOME-assisted project during the relevant period of affordability, with the

following exceptions:

o PJs can renew tenant-based rental assistance to families.

o PJs may provide tenant-based rental assistance to families that will occupy housing

previously assisted with HOME funds.

21 Chapter 1: Conduct Threshold Eligibility Review

o PJs may assist a homebuyer with HOME funds to acquire a unit that was previously

assisted with HOME funds.

• Acquisition of PJ-owned property. A PJ may not use HOME Program funds to reimburse

itself for property in its inventory or property purchased for another purpose. However, in

anticipation of a HOME project, a PJ may use HOME funds to:

o Acquire property

o Reimburse itself for property acquired with other funds, specifically for a HOME project.

• Project-based rental assistance. HOME funds may not be used for rental assistance if

receipt of funds is tied to occupancy in a particular project. Funds from another source, such

as a Housing Choice Voucher, may be used for this type of project-based assistance in a

HOME-assisted unit. Further, HOME funds may be used for other eligible costs, such as

rehabilitation, in units receiving project-based assistance from another source—for example,

Housing Choice Voucher or state-funded project-based assistance.

• Pay for delinquent taxes, fees, or charges. HOME funds may not be used to pay delinquent

taxes, fees, or charges on properties to be assisted with HOME funds.

HOME Project Requirements

The HOME Program is designed to provide affordable housing to low-income and very low-

income families and individuals. Therefore, the program has some key restrictions that are

designed to foster HUD’s commitment to long-term affordable housing, quality units, and

reasonable costs. These key restrictions include:

• Income eligibility and verification

• Occupancy and rent requirements

• Subsidy limits

• Affordability periods

• Property standards.

Chapter 1: Conduct Threshold Eligibility Review 22

Income Eligibility and Verification

Beneficiaries of HOME funds—homebuyers, homeowners, or tenants—must be low-income or

very low-income. A“low-income household” has an annual gross income that does not exceed 80

percent of area median income (AMI), as adjusted by household size. A “very low-income

household” has an annual gross income that does not exceed 50 percent of AMI, as adjusted by

household size.

Occupancy and Rent Requirements

In projects assisted with HOME funds, the HOME-assisted units must meet the occupancy and

rent requirements of the HOME Program. These requirements are explained in detail in Chapter

2.

Subsidy Limits

HOME establishes minimum and maximum amounts of HOME funds that may be invested in

any project. The minimum amount of HOME funds is $1,000 multiplied by the number of

HOME-assisted units in the project. The minimum relates only to the HOME funds, and not to

any other funds that might be used for project costs.

The maximum per unit HOME subsidy limit varies by PJ. Annually, HUD determines the

maximum amounts, which are based on HUD’s Section 221(d)(3) program limits for the

metropolitan area. These limits are available at the HOME Program website at

http://www.hud.gov/homeprogram/.

Affordability Periods

To ensure that HOME investments yield affordable housing over the long term, HOME imposes

rent and occupancy requirements for the duration of an affordability period. For homebuyer and

rental projects, the length of the affordability period depends on the amount of HOME assistance

to the project or buyer, and the nature of the activity funded. Throughout the affordability period,

income-eligible households must occupy the HOME-assisted housing.

Property Standards

HOME-funded properties must meet certain minimum property standards:

• State and local standards. State and local codes and ordinances apply to any HOME-funded

project regardless of whether the project involves acquisition, rehabilitation, or new

construction.

23 Chapter 1: Conduct Threshold Eligibility Review

• Model codes.

1

For rehabilitation or new construction projects where there are not state or

local building codes, the PJ must use one of the following three national model codes:

o Uniform Building Code (ICBO), National Building Code (BOCA), Standard Southern

Building Code (SBCCI)

Council of American Building Councils (CABO) one or two family code

Minimum Property Standards (MPS) in 24 CFR 200.925 or 200.926.

• Housing quality standards. For acquisition-only projects, if there are no state or local codes

or standards, the PJ must enforce Housing Choice Voucher Housing Quality Standards

(previously Section 8 HQS).

• Rehabilitation standards. Each PJ must develop written rehabilitation standards to apply to

all HOME-funded rehabilitation work. These standards are similar to work specifications,

and generally describe the methods and materials to be used when performing rehabilitation

activities.

• Uniform Federal Accessibility Standards. The UFAS standards apply to new construction

and substantially altered rehabilitation, in accordance with Section 504 of the Rehabilitation

Act of 1973.

• International Energy Conservation Code and Site and Neighborhood Standards, for

new construction projects.

HOME Administrative Requirements

HOME imposes certain administrative requirements related to the eligibility of administrative

and planning costs, match, and commitment and expenditure deadlines.

1

Since the promulgation of the HOME Program regulations, these code issuing agencies have merged to form the

International Code Council (ICC). The model codes used for the HOME Program are no longer being updated. In

their stead, the ICC has issued the International Building Code. HUD will consider whether changes to the HOME

regulations incorporating the International Building Code are appropriate. The HOME Program website provides

updated information on all HOME requirements. (See http://www.hud.gov/homeprogram/

.) For more information

about the International Building Code, see www.iccsafe.org.

Chapter 1: Conduct Threshold Eligibility Review 24

Administrative and Planning Costs

Each PJ may use up to 10 percent of each year’s HOME allocation for reasonable administrative

and planning costs. In addition, up to 10 percent of program income deposited in a PJ’s local

HOME account during a program year may be used for administrative and planning costs. PJs,

state recipients, and subrecipients may incur administrative and planning costs.

Match

The HOME Program requires that PJs contribute an amount equal to no less than 25 percent of

the total HOME funds drawn down in a year for project costs as a permanent contribution to

affordable housing. PJs incur a match obligation only for project funds, not for administrative,

operating, or capacity-building expenditures. Although the obligation is incurred per dollar

expended in the project, match credit can be invested in any HOME-eligible project, whether the

project receives HOME funds or not. Match funds can be contributed in many different forms,

including cash; value of waived taxes or fees; value of donated land or property; or donated

goods, services, materials, or equipment.

Commitment and Expenditure Deadlines

The HOME Program encourages PJs to expend their affordable housing funds expeditiously by

imposing two deadlines. HOME funds for a given program year must be committed to HOME

projects within two years of signing the HOME Investment Partnerships Agreement. For CHDO

set-aside funds, PJs must reserve funds for use by CHDOs within that 24-month period. In

addition, generally HOME funds must be expended within five years of receipt of funds. FY

2012 HOME funds must be spent within four years, in accordance with the Consolidated and

Further Continuing Appropriations Act of 2012 (P.L 112-55).

This section contains only a brief overview of the HOME requirements. For

additional information, PJs are encouraged to consult the HOME regulations and

the HOME Program website at http://www.hud.gov/homeprogram/.

1.2 Overview of the LIHTC Program

Before considering a HOME funding request for a project that has, or is expected to have,

LIHTCs, PJ staff should become familiar with what LIHTCs are and how the LIHTC program

works.

25 Chapter 1: Conduct Threshold Eligibility Review

What is a Low-Income Housing Tax Credit?

The U.S. Congress authorizes each state to allocate a certain number of Federal low-income

housing tax credits (LIHTCs) and issue up to a specified amount of tax-exempt bond financing

annually. The state’s allocation threshold is based on its population. Internal Revenue Service

rules found at Section 42 of the Internal Revenue Code (IRC, or “the Code”) govern the LIHTC

program. Each state establishes additional requirements and program priorities for the credits it

administers.

The state reserves LIHTCs for approved affordable housing projects that meet certain

affordability criteria for up to 30 years. These Federal tax credits are sold to investors as a way to

raise cash equity for eligible affordable housing projects. In exchange for cash up-front, the

investor receives a tax credit (dollar for dollar reduction in its Federal tax liability) each year for

a period of ten years. The IRS enforces compliance with the LIHTC affordability restrictions for

15 years. The LIHTC compliance period is the 15-year period during which a project must

continue to comply with the various LIHTC requirements to avoid any tax credit recapture. The

compliance period begins with the first taxable year in the credit period. The extended use

period is a date specified by either the LIHTC allocating agency or 15 years after the close of the

compliance period. During this extended period, the use of the property is restricted to affordable

low-income housing.

There are two forms of Federal LIHTCs, known as 9 percent and 4 percent tax credits. 9 percent

tax credits, also referred to as “70 percent present value LIHTCs,” are available for new

construction and rehabilitation. 4 percent tax credits, also referred to as “30 percent present value

LIHTCs,” are available for existing housing or federally subsidized housing and are generally

used in conjunction with tax-exempt bond financing. In an acquisition and substantial

rehabilitation project; the 4 percent credit is applied to the acquisition of the existing buildings

and the substantial rehabilitation qualifies for the 9 percent credits.

The LIHTC program has rent and occupancy standards that vary from those of the HOME

Program. The requirements for rents and occupancy under both the HOME and LIHTC programs

are detailed in Chapter 2.

State’s Role in the LIHTC Program

Each state allocating agency is required to issue a Qualified Allocation Plan (QAP) to document

how it plans to make the tax credits and tax-exempt bond financing available to developers. The

QAP is published annually. It contains vital information on the LIHTC program requirements

and the state’s funding preferences, in terms of the types of projects and locations in which it

Chapter 1: Conduct Threshold Eligibility Review 26

wishes to invest. Further, it explains the funding process, and identifies application deadlines and

when funding decisions (called reservations of credits) are made. Each state’s QAP typically

contains separate sections discussing the allocation procedures and requirements for 9 percent

LIHTCs and 4 percent LIHTCs.

Each state is required to conduct public hearings in the process of developing the QAP.

One key source of information for the PJ about the state allocating agency’s

funding priorities is the state LIHTC Qualified Allocation Plan (QAP). When PJs

know and understand the state’s LIHTC priorities, they can better target HOME

funds to projects that are the most fundable. Local PJs may also wish to discuss

rental housing priorities with state staff, through the formal public hearing process

on the QAP, and through other informal opportunities that arise.

Typical LIHTC Ownership Structures

Virtually all LIHTC projects are developed as single-asset entities, meaning that the ownership

entity has a single property in which all revenues, expenses, assets, and liabilities are accounted

for together.

LIHTC projects are typically owned by one of the following two types of legal entities:

• Limited liability corporations (LLCs). Limited liability corporations are similar to

partnerships. Typically one partner (or “member”) is designated as the “managing member”

who makes most day-to-day decisions. The tax credit investor member(s) typically is not

involved in day-to-day decision-making, but is involved in major decisions such as sales or

refinancing.

• Limited partnerships. Limited partnerships are similar to LLCs, except that the manager is

called the “general partner” and the investor(s) is called a “limited partner.” Some limited

partnerships have more than one general partner, in which case one of the general partners is

usually the managing general partner who makes most of the day-to-day decisions.

PJs should be aware of certain special conditions of ownership that apply if HOME CHDO set-

aside funds are being used in an LIHTC project. If the CHDO is applying and the ownership

structure is a limited partnership, the CHDO must be the managing general partner. If the

ownership is an LLC, a HUD waiver is required to allow for this ownership structure and the

CHDO must be the managing member of the LLC. Other ownership structures are possible in

theory, but are rarely seen in practice.

27 Chapter 1: Conduct Threshold Eligibility Review

Role of the LIHTC Investor

The state’s reservation of credits is not money from the state LIHTC allocating agency to the

developer. Instead, the allocation gives the owner the right to sell the reservation of LIHTCs to

an investor. The investor purchases the LIHTC allocation at a price determined by the market for

the credits for which the investor receives a 99 percent plus interest in the LLC or limited

partnership that will own the project. In exchange for the infusion of cash equity, the investor

receives its 99 percent ownership share plus the annual tax credits (a dollar for dollar reduction

against its Federal income tax liability) over the first ten years, followed by an additional five-

year affordability requirement, even though no additional tax credits may be claimed in those

years.

LIHTC Equity: “Syndicated” versus “Direct Investment”

Direct investment is the simplest form of LIHTC investment: a large corporation purchases the

entire investor interest in the project. By contrast, in a syndicated transaction, the investor

interest is purchased by a fund or investor pool composed of many investors. Syndicated

transactions are organized by LIHTC syndicators, who recruit corporate investors, create

investor funds / pools that appeal to a wide array of investors, and represent the investors for

purposes of getting the project funded, completed, leased-up, and operated in accordance with all

applicable compliance requirements.

The entity that applies for HOME funding is typically the owner, developer, or

sponsor of a project. Applicants for LIHTCs are generally referred to as “LIHTC

project sponsors.” Under LIHTC, this would typically be either the owner or

developer of the project. An LIHTC project sponsor is not the same as a sponsor

under the HOME Program. Under HOME, a sponsor is a community housing

development organization (CHDO) that works in partnership with another nonprofit

to develop and manage a property in certain circumstances. Unless otherwise

specified, this publication uses the term “owner” to refer to LIHTC project sponsors

as well as developers and sponsors of HOME projects.

9 Percent and 4 Percent LIHTCs

In terms of the requirements and how the credit works, there is little difference between a 9 and 4

percent LIHTC. Simply put, the 9 percent LIHTC leverages more equity for a project than a 4

percent LIHTC, and is therefore usually more desirable. An award of 9 percent LIHTCs typically

Chapter 1: Conduct Threshold Eligibility Review 28

generates sufficient investor equity proceeds to cover 50 to 90 percent of the cost to develop the

LIHTC units; whereas, an award of 4 percent LIHTCs typically generates investor equity

proceeds to cover only 20 to 40 percent of the cost to develop the LIHTC units.

The key differences between the two forms of Federal LIHTCs are summarized in Exhibit 1-1.

Competitive Allocation of 9 Percent LIHTCs

Because of the greater potential financial benefit of the 9 percent tax credit, these are in greater

demand, and are therefore allocated competitively, according to the state allocating agency’s

annual QAP. Typically, 9 percent LIHTC applications are received only once a year (although

some larger states might have more than one funding “round” to allocate credits.) Most state

allocating agencies use a point-scoring system to evaluate applications; this system is described

in the QAP. Some states create a pool of potential LIHTCs that are reserved for particular types

of projects (such as preservation projects in rural areas) or for particular types of sponsors (such

as nonprofit sponsors or public housing authorities). Within each pool, the highest-scoring

projects that meet all threshold requirements are selected to receive reservations of LIHTCs.

Tax-exempt bond financing cannot be used in conjunction with 9 percent LIHTCs.

Noncompetitive Allocation of 4 Percent LIHTCs

Because 4 percent credits are not in as high demand, most states accept LIHTC applications and

issue reservations on a noncompetitive basis year-round. However, 4 percent LIHTC

applications must still meet the state’s threshold requirements in order to be eligible to receive a

reservation of tax-exempt bond authority. Tax-exempt bond financing must be used in

conjunction with 4 percent LIHTCs. The associated tax-exempt bonds can be issued by any state

or local agency that has the legal authority to issue bonds (for example, a state housing finance

agency, a local public housing authority, or a local redevelopment agency).

For tax-exempt bond projects, there is an LIHTC requirement that at least 50 percent of the total

development cost be financed with tax-exempt bonds. Typically, the required amount of tax-

exempt bond financing is greater than the supportable first mortgage; in these situations, the

required amount of tax-exempt bonds are issued at the start of construction. Then, at the end of

the development period, some of the bonds are repaid (“redeemed”) so that the amount of the

remaining bonds matches the first mortgage loan amount.

29 Chapter 1: Conduct Threshold Eligibility Review

Exhibit 1-1: Summary of Key Differences in 9 and 4 Percent Tax Credits

9 Percent Credits

4 Percent Credits

Typical equity raised

50% to 90% of project’s total

development cost

20% to 40% of project’s total

development cost

Typical allocation process

Competitive allocation; one

time a year

Non-competitive allocation;

year-round

Typical use

New construction and

substantial rehabilitation

Moderate rehabilitation

How LIHTC Equity Is Calculated

The amount of LIHTC equity that can be secured for a project depends on a number of factors:

• Total development cost and how much of that cost is eligible under LIHTC

• Proportion of the project that will be LIHTC-assisted

• Type of LIHTC (9 or 4 percent)

• Price the LIHTC project sponsor is able to get for the credit.

Exhibit 1-2 illustrates the relationship of these variables and how the LIHTC equity is calculated.

Exhibit 1-2: Determining the LIHTC Equity

Total Development Costs

$6,400,000

Amount of Eligible Basis

$5,000,000

X Applicable Fraction

75%

= Qualified Basis

$3,750,000

+ 30% Basis Boost

$1,125,000

= Qualified Basis

$4,875,000

x LIHTC Percentage (9%)

x0.09

Chapter 1: Conduct Threshold Eligibility Review 30

= Annual Credit Amount

$438,750

X LIHTC Period

10 years

= Total LIHTC

$4,387,500

X Net Syndication Price

$ .75

= Net Syndication Proceeds (LIHTC

Equity)

$3,290,625

Total development cost. Total development cost is the total development budget (all

costs necessary to produce a finished, occupied project).

Eligible basis. Eligible basis is the amount of the development cost that is LIHTC-

eligible (excluding land and certain other costs that are not depreciable). This concept is

discussed in more detail in Chapter 2.

Applicable fraction. Applicable fraction represents the share of the property that is

LIHTC-assisted. It is based on the lesser of either: (1) the number of tax credit units to

the total number of units, or (2) the square footage of the tax credit units to the total

square footage of the property. Many tax credit projects have 100 percent tax credit units,

and these projects have an applicable fraction that is 100 percent. However, QAPs

increasingly favor mixed-income projects that include some market-rate units; mixed-

income projects have applicable fractions well below 100 percent.

Qualified basis. Qualified basis is eligible basis multiplied by the applicable fraction. In

other words, the portion of eligible basis that is attributable to the LIHTC units.

Basis boost percentage. Basis boost percentage is usually 100 percent. However,

projects located in HUD-designated qualified census tracts or difficult development areas

can be allocated up to 30 percent additional LIHTCs, at the discretion of the state LIHTC

allocating agency. (Note that the Housing and Economic Recovery Act of 2008 gave the

states’ housing finance agencies the right to determine which areas in their states could

be designated as difficult-to-develop areas.) If the full 30 percent addition is allocated,

the basis boost percentage is 130 percent. Basis boost may not be applied to acquisition

costs.

31 Chapter 1: Conduct Threshold Eligibility Review

LIHTC percentage. The LIHTC percentage represents the amount of credits that will be

generated by the qualified (and boosted) basis. The LIHTC percentage is published

monthly by the IRS, and is historically lower than the 9% or 4% factor. However, for

buildings placed in service through the end of 2013 the LIHTC percentage is fixed at

exactly 9 percent for the 9 percent LIHTC program, in accordance with changes made by

the Housing and Economic Recovery Act of 2008.

LIHTC period. The LIHTC period is the ten-year period over which the investor may

claim the LIHTCs. This is also sometimes referred to as the “credit period.” This is not

the same as the 15-year compliance period (the period during which the IRS can

recapture the tax credits from the investor for noncompliance with the affordability

restrictions.)

Total LIHTCs. Total LIHTCs equals the qualified basis multiplied by the LIHTC

percentage multiplied by ten years. This is the total dollar amount of LIHTCs that the

owner is expected to receive over the ten-year credit period.

Net syndication price. Net syndication price is the amount that the LIHTC investor

pays for $1.00 of Federal income tax credit. Historically, the net syndication price

typically ranged from 70 cents to 90 cents. (This means that the investor is willing to pay

70 to 90 cents today for every $1.00 of anticipated tax credit that it will receive later.) In

the mid-2000s, the typical price rose above 90 cents, only to drop significantly beginning

in 2008. At this publication, net syndication prices are volatile and are most often

reported toward the low end of the historical range.

Net syndication proceeds. Net syndication proceeds are the total dollar amount that the

LIHTC investor pays the LIHTC project sponsor. It is based on the total project credit

amount multiplied by the net syndication price. In this example, the net syndication

proceeds are sufficient to pay for 51 percent of total development cost.

Market Trends in LIHTC Equity Prices

Historically LIHTC prices have been stable and there has been an adequate market of potential

LIHTC investors. As a result, developers had high confidence that an LIHTC reservation could

readily be converted into LIHTC equity. However, financial upheaval in 2008 created significant

stress in the LIHTC equity market, demonstrating that there can be unpredictability in this

market.

Chapter 1: Conduct Threshold Eligibility Review 32

In summary, many of the largest LIHTC investors lost confidence that the business environment

would be profitable. Without anticipated profits, there would be no Federal income taxes; and

without tax liability, there would be no need for credits. The market stopped purchasing LIHTCs.

This has had two primary results:

• LIHTC prices became (and continue to be) unstable.

• Some LIHTC projects have been unable to find an investor—particularly those with less-

experienced or less financially-sound developers, large projects (over 200 units), projects in

rural areas, projects with especially complex financial and compliance structures, and

projects in areas of or declining population.

Recent market trends dictate that the PJ understand that the demand for tax credits can change

over time; one cannot assume there will always be a supply of investors. PJs should discuss this

issue with the state allocating agency when making decisions about funding tax credit projects.

In addition, PJ underwriters should consider the following:

• Currently, pre-2008 benchmarks for LIHTC equity prices are not reliable.

• Developers today are under pressure to propose projects that are less complex and that

involve fewer risks, as compared to the types of projects that could readily find LIHTC

investors prior to 2008.

• There is a greater need for flexibility, creativity, and professionalism by PJs in working with

the state and with developers.

LIHTC Deadlines

There are three primary deadlines in the LIHTC program:

• Allocation and reallocation deadlines

• “Carryover” requirement

• Placed in service requirement.

Allocation and Reallocation

The state has two years to make an initial allocation (reservation) of LIHTCs. If a developer

returns its LIHTC reservation, the state has two additional years to reallocate the LIHTCs to

another project.

33 Chapter 1: Conduct Threshold Eligibility Review

Carryover Requirement

Once the state makes an initial reservation of LIHTCs for a project, the developer must incur 10

percent of the reasonably expected eligible basis within 12 months of when the LIHTC

reservation was made. This is called the carryover requirement. Although 10 percent must be

spent, the expenditures need not be for basis-eligible items. Once this threshold is achieved, the

developer receives a “carryover allocation” from the state; that is, the state allocates the

remaining credits to the project. If the developer is unable to spend 10 percent of the reasonably

expected eligible basis within 12 months, the project loses the credits and they are reallocated by

the state to another project. (Note: the Housing and Economic Recovery Act of 2008 extended

this expenditure deadline from six months.)

“Placed In Service” Requirement

The LIHTC program does not have a deadline for full expenditure of funds like the HOME

Program, but it has a deadline for project occupancy, called “placed in service.” The state LIHTC

allocating agency and the IRS track LIHTC projects at the building level. A new construction

LIHTC building is placed in service when construction has been completed and when the first

unit in the building is certified as suitable for occupancy under state or local law (see IRS Notice

88-116). Rehabilitated LIHTC buildings are considered to be placed in service at the close of any

24-month period – selected by the taxpayer – over which the rehabilitation expenditures are

aggregated. LIHTC buildings must be placed in service no later than December 31 of the second