Home Equity Lending Matrices (HELOC)

Home Equity Lines of Credit

Release Date: 9/12/2022

Minimum FICO

Max HCLTV

Owner

Occupied

2

nd

Home Investment

FICO / CLTV /

Occupancy Maximums

740+ 90% 80%

700-739 90% 80%

680-699 80%

Product Terms

• 30-year variable term (Index plus a margin)

• 10-year interest only draw period with a 20-year fully amortizing repayment period

Initial Draw

• Minimum $50k

Additional Draws

• Prohibited during the first 90 days following closing date

• Minimum $1000 not to exceed credit limit

Index

• Prime Rate as published in the WSJ on the 1st of the month, if there is a range published the highest rate will be used

Lifetime Rate Cap /

Floor

• Lifetime Cap = 18.00% unless prohibited by law

• Floor Rate = 4.00%

Debt to Income

• Max 45% DTI

• 30 year, fully amortized payment based on start rate + 2% and the total credit limit used to qualify

Line Amount

• Minimum Line amount $50,000

• Maximum Line Amount $500,000

• **Owner Occupied max total financing is limited to $3,000,000 (total amount of 1

st

and 2

nd

lien combined)**

• **2

nd

Home max total financing is limited to $2,000,000 (total amount of 1

st

and 2

nd

lien combined)**

Occupancy

• Owner-Occupied

• Second Homes

Piggyback Additional

Requirements

• Final Approval from first lien lender showing all conditions met

• Final Closing Disclosure from first lien to confirm final CLTV and DTI calculation

• Title policy from first lien transaction should be used and must include title insurance/CPL/Wire Instructions

• Use of existing appraisal from first lien is acceptable subject to collateral desk review (CDA) *See Appraisal Requirements

section below

• Agreement of sale on purchase transactions

Correspondent Only:

• Final DU/LP Findings are required to be provided from the 1

st

mortgage lender (If no DU/LP Findings are provided,

guidelines will follow Spring EQ’s Home Equity Underwriting Guidelines).

Wholesale Only:

• Spring EQ to perform closing agent validation audit prior to closing

• Initial and Final DU/LP Findings are required to be provided from the 1

st

mortgage lender (If no DU/LP Findings are

provided, guidelines will follow Spring EQ’s Closed End Home Equity Guidelines).

Appraisal

Requirements

• Loan Amounts < $250,000 any of the following options are permitted:

o AVM with exterior property inspection with the following requirements:

Max 90% CLTV

Correspondent Only: See Seller Guide for AVM eligibility & Approved Vendors

o Prior Use Appraisal (See below requirements)

o Drive By Appraisal

Wholesale Only: Spring EQ to order with UW Approval

Correspondent: Must be ordered through the following Approved Vendors & Products: Accurate

Group – Valunet Plus, Valuation Connect – Equity Connect Report (ECR)

o Full Interior Appraisal (1004/1025/1073)

• Loan amounts >= $250,000

o Full Interior Appraisal (1004/1025/1073)

o Prior Use Appraisal (See below requirements)

• Recertification of a prior use appraisal is acceptable when the following requirements are met:

o Report has been completed within 12 months of settlement date

o Current appraisal provided must be on form 1004(Single family), 1025(multi-family), or 1073(Condo)

o Original Appraisal must be “AS IS”

o A Desktop Review and Property Condition Report are required and will be ordered by Spring EQ to validate any

use of a prior use appraisal

Desktop Review Risk Score must be low or moderate with no additional review recommended by

reviewer

Desktop Review commentary contains no comments that adversely impact value, marketability, or

Home Equity Lending Matrices (HELOC)

condition of the property

Desktop Review Home Data Index must support either a neutral or increasing market trend

Wholesale Only: CDA & PCI will be ordered by Spring EQ to validate the use of an existing appraisal

o CLTV will be calculated as the lower of the Purchase Price/Desktop Review value or the appraised value

Wholesale Only:

When a full appraisal is required, the order is to be placed by Broker https://www.clearcapital.com/spring‐eq/ and

may not be

ordered until the borrower has e‐signed their intent to proceed.

Income

• Refer to Spring EQ Home Equity Underwriting Guidelines for comprehensive list of income

types

• Income calculation must comply with all Appendix Q requirements as required in the ATR Final Ruling

Self-Employed

• For Self-Employed borrowers the following documentation will be required for qualification:

o Most Recent 2 Years Personal and Business Federal Tax Returns along with transcripts (with the most recent

year not being older than 2020)

o YTD Profit and loss and balance sheet for the most recent month end preceding the application date

o Tax Transcripts

*For example, if you have an application date of 8/10/2021, the P&L and Balance sheet must be inclusive of the

business activity thru 7/31/2021

o Declining Income:

Income declining more than 20% is now permitted with the following requirements

• Most recent 12-month average must be used to calculate the income

• DTI cannot exceed 40%

*Note declining income requirement is limited to self-employed borrowers only and is not intended to be applied

when variable bonus/commission income is used

Wholesale Only:

• Tax Transcripts are required unless income is validated using an automated VOI such as WorkNumber (etc)

Ineligible Senior Lien

• Senior liens with high-risk features which can include, but are not limited to:

o Loans in active forbearance or deferment

o Negative Amortization

o Balloon, if the balloon payment becomes due during the amortization period of our new 2nd lien

**Balloon terms that resulted from a modification are acceptable so long as all requirements in the modification

section are met

o Reverse Mortgages

o Interest Only Mortgages

o Private Mortgages opened within the past 12 months

Age of Documents

• Expiration Dates are based on the Note Date of the Loan:

o Credit Documents (Income/Asset/Credit report) – 60 Days

o Collateral - 90 days

o Title - 90 Days

o Appraisal – 90 Days

For Appraisals > 90 Days, Recertification of the original Appraisal is required

Credit Score

• The credit score used to qualify will be based on a single Experian (version 8) repository score – The lowest of all

borrowers’ scores

• A credit score must be available; non-traditional credit not permitted

Correspondent Only:

• Tri-Merge Credit Score meeting GSE guidelines will be acceptable

• Lender may only choose Experian 8 or Tri-Merge on setting up of relationship

Trade lines

• Minimum of three trade lines are required for all borrowers that are contributing income to qualify. At least one trade line

must be open and active for the past 12 months.

• A current mortgage paid as agreed for past 36 months will override the minimum trade line requirement

Housing History

• Max 0x30x24 inclusive of all mortgages and all REO for all borrowers on the transaction (No late payments in the past 24

months)

• For Purchase transactions 12 months rental history verification is required

• IF VOM/VOR is from a private party, cancelled checks or bank statements are required

• The first mortgage loan cannot be in any active deferment or forbearance period. Once the deferment or forbearance

period has expired, a minimum of three-monthly payments at the current payment must be documented

Employment/Income

Verification

• Piggybacks: Follows DU/LP findings; however, they must adhere to current Fannie Mae income/employment requirements

• Standalones: Will follow Spring EQ’s Home Equity Underwriting Guidelines

Significant Derogatory

Credit

• Measured from the Disbursement Date

• Period of time that must elapse prior to loan eligibility is as follows:

o Foreclosure - 7 years

o Charge-Off of a Mortgage Account, Deed-in Lieu, Pre-foreclosure Sale or Short Sale - 4 years

o Restructured or Short Payoff of a mortgage secured by a property other than the subject- 4 Years

o Chapter 7 or 11 Bankruptcy - 4 years from discharge or dismissal

Home Equity Lending Matrices (HELOC)

o Chapter 13 Bankruptcy- 2 years from discharge or 4 years from dismissal

• Multiple events within the past 7 years are not permitted and both events must be greater than 7 years

Seasoning

• No seasoning is required subject to the following:

o Seasoning 0-6 Months – Must use the lower of the purchase price or appraised value

o Seasoning > 6 Months – May use appraised value

Liabilities

• Paying off debt to qualify is permitted (Paying down debt to qualify is not permitted)

• Lease payments are not permitted to be excluded

• Student loan – 1% of the balance is used to calculate the payment to qualify when there is no payment reporting

Ineligible Property

Types

• Cooperatives

• Condotels (Refer to the Non-Warrantable Condo)

• New Construction Condominium Projects

• Hotel/Motel Condominiums

• Mobile Homes

• Manufactured Housing

• Commercial Operations

• Geodesic Domes

• Working farms and ranches

• Unimproved Land

• Properties with >20 Acres

• Timeshares

• Leasehold

• 2-4 Unit Properties

• Properties listed for sale

in the past 12 months

Eligible Property

Types

• Single Family

• PUDs

• Modular homes (as defined by Fannie Mae)

• Condominiums

Condominiums

• Established projects only

• Online search for no condotel or short-term rental

• If Master Condominium insurance policy does not contain walls-in coverage, an H06 policy is required

Title Insurance

• Loan amount less than $250,000: Owner and Encumbrance Property Report

• Loan amount greater than or equal to $250,000: Full Title is required

Wholesale Only:

• Spring EQ to order all title work

• For piggyback transactions:

o Title insurance and CPL are required for the Spring EQ proposed loan

o Spring EQ requires risk review to be completed by Secure Insight to validate the settlement agent

(Mtgee Clause- Spring EQ LLC, ISAOA/ATIMA, 100 W Matsonford Rd Bldg 5 Ste 100, Radnor, PA 19087-4559)

Correspondent Only:

• For piggyback transactions:

o Title insurance and CPL are required

Homeowners

Insurance

• Existing coverage amount must be equal to the lesser of the following:

o 100% of the insurable value of the improvements, as established by the property insurer; or

o the unpaid principal balance of the all existing liens against the subject property, plus the new HELOC Max Line

Amount

Solar Panel UCC

• UCC Filings do not need to be calculated in the CLTV with the following documentation:

• Copy of account statement to ensure obligation is accounted for in the DTI if not reporting on credit

**NOTE: UCC filings that are paid through tax assessments (such as HERO and PACE loans) are not eligible and must be

paid in full with proceeds.**

Ineligible Borrowers

• Non-Occupant co-borrowers are not permitted

• Vesting is not permitted to be in the name of an LLC, corporation, or partnership

• Power of Attorney is limited to Piggyback Purchases only and must follow GSE Requirements

• Irrevocable Trusts are not permitted

Assumptions

• Loans are not assumable

Prepayment Penalty

• Not permitted

Escrows

• Not permitted

Retail Lien Positions &

States

• 1

st

, 2

nd

Liens

• 1

st

Lien only available in the following states:

o AL, AZ, CA, CO, CT, DE, FL, GA, IA, IL, KS, KY, MD, ME, MI, MN, MS, NC, NH, NJ, OH, OK, OR, RI, SC, TX, VA,

VT, WI

o 1

st

Lien HELOC Not Allowed in the Following State: PA, TN

o 1

st

Lien HELOC can not be used for Purchase Transactions

• 2

nd

Lien available in all states except

o AK, HI, ID, MA, MO, ND, NV, NY, SD, WA, WV, WY, UT

Wholesale Lien

Positions & States

• 1

st

, 2

nd

Liens

• 1

st

Lien only available in the following states:

o AL, AZ, CA, CO, CT, DE, FL, GA, IA, IL, KS, KY, MD, ME, MI, MN, MS, NC, NH, NJ, NV, OH, OK, OR, RI, SC, TX,

UT, VA, VT, WI

Home Equity Lending Matrices (HELOC)

o 1

st

Lien HELOC Not Allowed in the Following State: PA, TN

o 1

st

Lien HELOC can not be used for Purchase Transactions

• 2

nd

Lien available in all states except

o AK, HI, ID, MA, MO, ND, NY, SD, TN, WA, WV, WY

Transaction Types

• Arm’s Length Transactions

• Not Permitted - Non-Arm’s Length Transactions –

A Non-Arm's length transaction, also known as an arm-in-arm transaction, refers to a business deal in which buyers and

sellers have an identity of interest; in short, buyers and sellers have an existing relationship, whether business-related or

personal.

**Spring EQ does not allow these transactions with the exception of a tenant buying the property that they are currently

renting; from the landlord/owner of the property. All other Non-Arm's Length Transactions are ineligible for financing.

3

rd

Party Estimated of

Fees

Wholesale Only:

https://www.wholesale.springeq.com/fees/

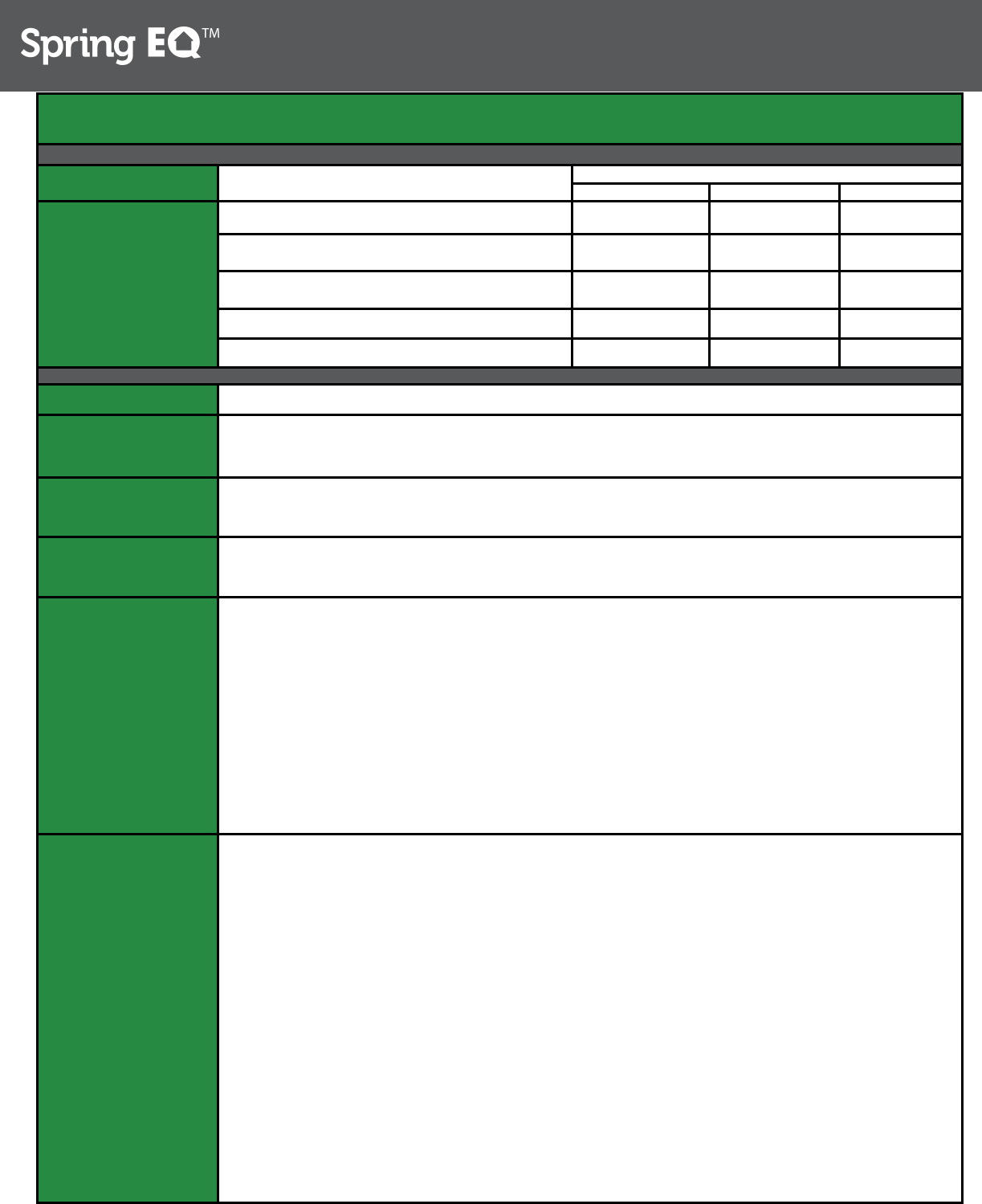

Home Equity Lending Matrices (Fixed Rate)

Fixed Rate Home Equity

Release Date: 9/12/2022

Minimum FICO

Max CLTV

Owner Occupied

2

nd

Home

Investment

FICO / CLTV /

Occupancy Maximums

740+ 95% 90% 85%

700-739 95% 90% 85%

680-699 90% 90% 85%

640-679 85% 80% 80%

620-639 70% 60% 60%

Terms

• Stand-Alone Second Liens and Piggybacks

• Fixed rate terms: 5, 10 ,15, 20, 25 & 30 years

Debt to Income

• Max 50% DTI with Minimum 700 FICO Score and $3,500 of Monthly Residual Income

o Monthly Residual Income = Total Monthly Income – Total Monthly Mortgage and Non-Mortgage Obligations

listed in the Underwriting Guidelines

• Max 45% DTI for all other scenarios

Loan Amount

• Minimum Loan amount $25,000

• Maximum Loan Amount $500,000

• **Owner Occupied max total financing is limited to $3,000,000 (total amount of 1

st

and 2

nd

lien combined)**

• **2

nd

Home & Investment max total financing is limited to $2,000,000 (total amount of 1

st

and 2

nd

lien combined)**

Occupancy

• Owner-Occupied

• Second Homes

• Investment Properties

o Limited to 10 Financed Properties

Piggyback Additional

Requirements

• Final Approval from first lien lender showing all conditions met

• Final Closing Disclosure from first lien to confirm final CLTV and DTI calculation

• Title policy from first lien transaction should be used and must include title insurance/CPL/Wire Instructions

• Use of existing appraisal from first lien is acceptable subject to collateral desk review (CDA) *See Appraisal Requirements

section below

• Agreement of sale on purchase transactions

Correspondent Only:

• Final DU/LP Findings are required to be provided from the 1

st

mortgage lender (If no DU/LP Findings are provided,

guidelines will follow Spring EQ’s Home Equity Underwriting Guidelines).

Wholesale Only:

• Spring EQ to perform closing agent validation audit prior to closing

• Initial and Final DU/LP Findings are required to be provided from the 1

st

mortgage lender (If no DU/LP Findings are

provided, guidelines will follow Spring EQ’s Closed End Home Equity Guidelines).

Appraisal

Requirements

• Loan Amounts < $250,000 any of the following options are permitted:

o AVM with exterior property inspection with the following requirements:

Max 95% CLTV

No Higher Priced Mortgage Loans (HPMLs)

Correspondent Only: See Seller Guide for AVM eligibility & Approved Vendors

o Prior Use Appraisal (See below requirements)

o Drive by Appraisal (DTI <= 43% required)

Wholesale Only: Spring EQ to order with UW Approval

Correspondent: Must be ordered through the following Approved Vendors & Products: Accurate

Group – Valunet Plus, Valuation Connect – Equity Connect Report (ECR)

o Full Interior Appraisal (1004/1025/1073)

• Loan amounts >= $250,000

o Prior Use Appraisal (See below Requirements)

o Full Interior Appraisal (1004/1025/1073)

• Recertification of a prior use appraisal is acceptable when the following requirements are met:

o Report has been completed within 12 months of settlement date

o Current appraisal provided must be on form 1004(Single family), 1025(multi-family), or 1073(Condo)

o Original Appraisal must be “AS IS”

o A Desktop Review and Property Condition Report are required and will be ordered by Spring EQ to validate any

use of a prior use appraisal

Desktop Review Risk Score must be low or moderate with no additional review recommended by

reviewer

Desktop Review commentary contains no comments that adversely impact value, marketability, or

condition of the property

Home Equity Lending Matrices (Fixed Rate)

Desktop Review Home Data Index must support either a neutral or increasing market trend

Wholesale Only: Desktop Review & Property Condition Report will be ordered by Spring EQ to

validate the use of an existing appraisal

o CLTV will be calculated as the lower of the Purchase Price/Desktop Review value or the appraised value

Wholesale Only:

• When a full appraisal is required, the order is to be placed by Broker https://www.clearcapital.com/spring‐eq/ and

may

not be ordered until the borrower has e‐signed their intent to proceed.

Income

• Refer to Spring EQ Home Equity Underwriting Guidelines for comprehensive list of income

types

• Income calculation must comply with all Appendix Q requirements as required in the ATR Final Ruling

Self-Employed

• For Self-Employed borrowers the following documentation will be required for qualification:

o Most Recent 2 Years Personal and Business Federal Tax Returns along with transcripts (with the most recent

year not being older than 2020)

o YTD Profit and loss and balance sheet for the most recent month end preceding the application date

o Tax Transcripts

*For example, if you have an application date of 8/10/2021, the P&L and Balance sheet must be inclusive of the

business activity thru 7/31/2021

o Declining Income:

Income declining more than 20% is now permitted with the following requirements

• Most recent 12-month average must be used to calculate the income

• DTI cannot exceed 40%

*Note declining income requirement is limited to self-employed borrowers only and is not intended to be applied

when variable bonus/commission income is used

Wholesale Only:

• Tax Transcripts are required unless income is validated using an automated VOI such as WorkNumber (etc)

Ineligible Senior Lien

• Senior liens with high-risk features which can include, but are not limited to:

o Loans in active forbearance or deferment

o Negative Amortization

o Balloon, if the balloon payment becomes due during the amortization period of our new 2nd lien

**Balloon terms that resulted from a modification are acceptable so long as all requirements in the modification

section are met

o Reverse Mortgages

o Private Mortgages opened within the past 12 months

o Interest Only Mortgages

Assumptions

• Loans are not assumable

Age of Documents

• Expiration Dates are based on the Note Date of the Loan:

o Credit Documents (Income/Asset/Credit report) – 60 Days

o Collateral - 90 days

o Title - 90 Days

o Appraisal – 90 Days

For Appraisals > 90 Days, Recertification of the original Appraisal is required

Credit Score

• The credit score used to qualify will be based on a single Experian (version 8) repository score – The lowest of all

borrowers’ scores

• A credit score must be available; non-traditional credit not permitted

Correspondent Only

• Tri-Merge Credit Score meeting GSE guidelines will be acceptable

• Lender may only choose Experian 8 or Tri-Merge on setting up of relationship

Trade lines

• Minimum of three trade lines are required for all borrowers that are contributing income to qualify. At least one trade line

must be open and active for the past 12 months.

• A current mortgage paid as agreed for past 36 months will override the minimum trade line requirement

Housing History

• Max 0x30x24 inclusive of all mortgages and all REO for all borrowers on the transaction (No late payments in the past 24

months)

• For Purchase transactions 12 months rental history verification is required

• **IF VOM/VOR is from a private party, cancelled checks or bank statement are required**

Seasoning

• 0-6 Months – Lower of the purchase price or appraised value must be used to calculate the CLTV

• >6 Months Seasoning – No restrictions

• 6 Month Seasoning is required for all Investment Properties

Significant Derogatory

Credit

• Measured from the Disbursement Date

• Period of time that must elapse prior to loan eligibility is as follows:

o Foreclosure - 7 years

o Charge-Off of a Mortgage Account, Deed-in Lieu, Pre-foreclosure Sale or Short Sale - 4 years

o Restructured or Short Payoff of a mortgage secured by a property other than the subject- 4 Years

o Chapter 7 or 11 Bankruptcy - 4 years from discharge or dismissal

o Chapter 13 Bankruptcy- 2 years from discharge or 4 years from dismissal

Home Equity Lending Matrices (Fixed Rate)

o Multiple events within the past 7 years are not permitted and both events must be greater than 7 years

Liabilities

• Paying off debt is to qualify is permitted

• Lease payments are not permitted to be excluded

• Student loan – 1% of the balance is used to calculate the payment to qualify when there is no payment reporting

Eligible Property

Types

• Single Family (including Modular homes and PUD’s)

• Condominiums (Fannie Mae Warrantable)

• 2-Unit

Ineligible Property

Types

• Cooperatives

• Condotels (Refer to the Non-Warrantable Condo)

• New Construction Condominium Projects

• Hotel/Motel Condominiums

• Mobile Homes

• Manufactured Housing

• Commercial Operations

• Geodesic Domes

• Working farms and ranches

• Unimproved Land

• Properties with >20 Acres

• Timeshares

• Leasehold

• 3-4 Units

• Properties listed for sale

in the past 12 months

Condominiums

• Established projects only

• Online search for no condotel or short-term rental

• If Master Condominium insurance policy does not contain walls-in coverage, an H06 policy is required

Title Insurance

• Loan amount less than $250,000: Owner and Encumbrance Property Report

• Loan amount greater or equal to than $250,000: Full Title is required

Wholesale Only:

• Spring EQ to order all title work

• For piggyback transactions:

o Title insurance and CPL are required for the Spring EQ proposed loan

o Spring EQ requires risk review to be completed by Secure Insight to validate the settlement agent

(Mtgee Clause- Spring EQ LLC, ISAOA/ATIMA, 100 W Matsonford Rd Bldg 5 Ste 100, Radnor, PA 19087-4559)

Correspondent Only:

• For piggyback transactions:

o Title insurance and CPL are required

Homeowners

Insurance

• Use of existing coverage amount is permitted. Replacement cost estimator or increases in coverage are not required

regardless of outstanding lien amounts

Solar Panel UCC

• UCC Filings do not need to be calculated in the CLTV with the following documentation:

o Copy of account statement to ensure obligation is accounted for in the DTI if not reporting on credit

o **NOTE: UCC filings that are paid through tax assessments (such as HERO and PACE loans) are not eligible

and must be paid in full with proceeds.**

Recently Listed

Properties

• Properties listed for sale in the past 12 months are not eligible

Ineligible Borrowers

• Non-Occupant co-borrowers are not permitted

• Vesting is not permitted to be in the name of an LLC, corporation, or partnership

• Power of Attorney is limited to Piggyback Purchases only and must follow GSE Requirements

•

Properties Titled in a Trust are not Permitted

Prepayment Penalty

• Not Permitted

Escrows

• Not required

Retail Lien Positions &

States

• 2

nd

Lien Only

• 2

nd

Lien available in all states except

o AK, HI, ID, MA, MO, ND, NV, NY, SD, WV, WY, UT

Wholesale Lien

Positions & States

• 2

nd

Lien Only

• 2

nd

Lien available in all states except

o AK, HI, ID, MA, MO, ND, NY, SD, WV, WY

Correspondent Lien

Positions & States

• 2

nd

Lien Only

• 2

nd

Lien available in all states except

o AK, HI, ID, MA, MO, ND, NV, NY, OR, RI, SD, VT, WV, WY

• Non-Delegated Underwrite not available in: WA

Transaction Types

• Arm’s Length Transactions

• Not Permitted - Non-Arm’s Length Transactions –

A Non-Arm's length transaction, also known as an arm-in-arm transaction, refers to a business deal in which buyers and

sellers have an identity of interest; in short, buyers and sellers have an existing relationship, whether business-related or

personal.

**Spring EQ does not allow these transactions with the exception of a tenant buying the property that they are currently

renting; from the landlord/owner of the property. All other Non-Arm's Length Transactions are ineligible for financing.

Home Equity Lending Matrices (Fixed Rate)

Disaster Policy

• Please refer to the list of affected counties published by FEMA using the following link: http://www.fema.gov/disasters

• Prior to closing, Spring EQ will require a property inspection for any loan secured by a property in the affected area where

individual

• Assistance was provided. If the subject property is located in one of the impacted counties and the collateral valuation

was completed prior to the incident period end date, Spring EQ will require a post disaster inspection confirming the

property was not adversely affected by the disaster.

Estimated 3

rd

Party

Fees

Wholesale Only:

• https://www.wholesale.springeq.com/fees/