Fiscal union and the need

for accurate

macroeconomic statistics

Guntram Wolff, Bruegel

Luxembourg 26 Jan 2016

Outline

2

The euro area crisis

The new institutional setup

Importance of macroeconomic statistics

Towards fiscal union

Creative fiscal accounting

Heterogeneity of accounting standards in

Europe

Timeline of events

Source: Bruegel based on Datastream

10-year government bond yields (%)

0

5

10

15

20

25

30

35

40

Belgium Germany Ireland Greece Spain France Italy Portugal

QE

Lehman

collapse

Debt

crisis

ESM signed

European Council

announcement on

BU

Speech by

Mario Draghi

Slide 3

1

Instead of using OMT date, please show date of Draghi speech in London. For BU, please show that Eurpean Council announcement "We break

the vicious circle between banks and sovereigns."

Guntram Wolff;

1

sure

Uuriintuya Batsaikhan;

Measuring competitiveness divergence

4

80

85

90

95

100

105

110

115

120

125

130

Germany Ireland Greece Spain

France Italy Belgium Portugal

ULC-based real effective exchange rates (vs. EA18)

Source: ECFIN

Source: Bruegel based on AMECO, Eurostat

-300

-200

-100

0

100

200

300

400

Current account balance (in bn EUR)

Spain Italy Germany France Euro area

Current account statistics

European Stability Mechanism (ESM)

Treaty on Stability, Coordination and Governance in

the Economic and Monetary Union (TSCG)

Sixpack

Banking Union (BU)

OMT programme

5 Presidents’ Report further proposes:

Advisory European Fiscal Board (stage 1)

Euro area stabilization function (stage 2)

Key governance decisions already taken

The new EU fiscal framework puts more

emphasis on the so-called „structural“ deficit

It is computed with GDP and „potential“ GDP

data

Well established empirical finding that GDP

revisions are significant (see real-time

literature, Cimadomo 2011 survey)

Macroeconomic statistics clearly matter for

fiscal policy decision making

Fiscal framework and macroeconomic

statistics

7

Real – time errors in budget procedure.

8

It is part of 6 pack

Significant emphasis on concept of

„competitiveness“

Growing literature on the need to measure

competitiveness with micro-economic data.

Macroeconomic Imbalances Procedure

9

Fiscal Union?

10

Ratio of local to general government expenses in 2013 (%)

Source: IMF, Government Finance Statistics

Note: Federal countries in dark blue.

Fiscal policy is basically national.

Musgrave and Musgrave (1989):

Purpose of budget

• Finance public goods common to all federal states

• Correct geographical and historical disadvantages,

maintain national cohesion

• Smooth business fluctuations

expand or re-orient EU budget?

complement EU and national spending with

spending at different levels (EA, Schengen)?

In EA, case for fiscal stabilization is strongest,

allocation and distribution not primarily EA issues

Fiscal Union: Basics

11

Capital and credit market channel by far the

most important ones

Stabilization channels

12

Source: IMF (2013)

Creation of sizeable federal budget not

realistic given the degree of political and

social integration of the EU…

Need for fiscal policy coordination

• Interaction between monetary and fiscal policies

• Fiscal policy may supplement monetary policy

• Direct cross-border effects of national fiscal policy

Has been unsatisfactory so far (see next

slide)

Stabilization through National Budgets

13

Stabilization through National Budgets

14

Fiscal impulse (% of GDP) and discretionary fiscal policy (% of potential GDP) in EA

Source: AMECO and own calculations

Notes: Crisis: countries under ESM programme; SGP: countries under

corrective or preventive arm

15

0,00

0,25

0,50

0,75

1,00

2011 2012 2013 2014

21 EU

countries

14 Euro-

area

countries

7 Non-euro

area

countries

European Semester Reform Index

Source: Darvas and Leandro (2015)

European Semester and Policy Coordination

Authors also show that implementation of

recommendations not better than in the case of OECD

recommendations

More pressure to reduce the debt ratio in normal and

good times to allow for fiscal stabilization in bad

times

Potential debt restructurings to prevent overly-harsh

austerity and make rules more credible

• Complete Banking Union with incentive to diversify banks’

exposure to sovereign risk

• Deposit guarantee scheme with common fiscal backstop

• ESM as firewall in case of sovereign debt restructuring

Important role of European Fiscal Board

But conundrum of shared sovereignty

remains

National Fiscal Policies

16

Flexibility of SGP rules in bad times (for the

short term)

• European Fiscal Board

• National adjustment accounts

But avoid fuzzy discretion

Need to coordinate a fiscal stance, in

particular at Zero Lower Bound

National Fiscal Policies

17

Fiscal rules aim at constraining government behaviour

To circumvent such rules governments sometimes revert to

creative accounting

Empirical evidence of creative accounting in the EU (von Hagen

and Wolff, 2004):

• SGP rules have induced governments to use stock-flow adjustments to hide

deficits

• Tendency to substitute stock-flow adjustments for budget deficits is strong for the

cyclical component of the deficit (as in times of recession the cost of reducing the

deficit is particularly large)

The amount of creative accounting depends on the reputation cost

for the government and the economic cost of sticking to the rule

Again points to the importance of quality statistics

Creative accounting

18

The closer we get to fiscal union, the more

high quality and harmonized data is needed

• Base for fiscal rules and policy recommendation

• Limit procylicality of current fiscal policy

• Identification of good and bad times

It is about national policies and data

Address circumvention of rules through

creative accounting

Implications for Public Sector Accounting

19

Complex and heterogeneous

• Cash basis vs. accrual accounting?

• Federal systems often exhibit the most complicated systems, as different

federal regions stick to different accounting principles

Accounting systems in Europe

At the central

level

Regional level municipality level Social

insurance

Accrual accounting 12 2 14 13

Modified accrual accounting 5 - 4 4

Combination between accrual

accounting and cash basis

5 1 7 4

Cash basis 4 - - 1

Not applicable - 23 - 1

No answer 1 1 2 4

Total 27 27 27 27

Source: Ernst&Young, European Commission

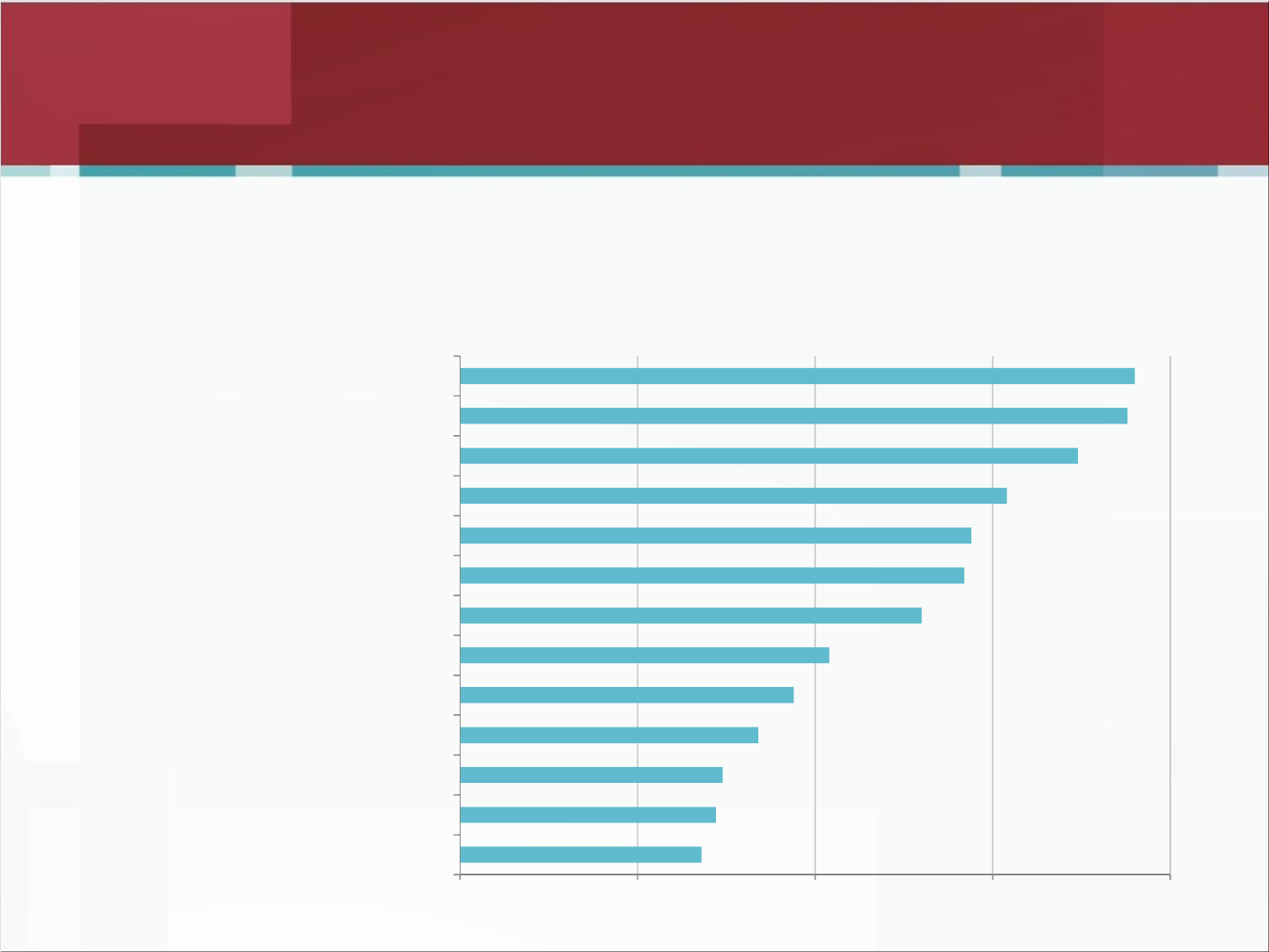

Conformity to IPSAS?

• A Ernst&Young study reveals how similar accounting systems in the single EU

member states are to the IPSAS

• Result: the conformity ranges from 30% to 90%

Accounting systems in Europe (i)

Source: Ernst&Young, European Commission

0 25 50 75 100

Germany (Cash basis in government sector)

Ireland (central government)

Malta (central government)

The Netherlands (central government)

Italy (central government)

Austria (Federal state)

Belgium (central government)

Denmark (central government)

Finland (central government)

Spanien (government sector)

France (central government)

Sweden (central government)

United Kingdom

Fiscal policy making is at the heart of

European crisis response.

It requires adequate macroeconomic

information

The more „fiscal union“ advances, the more

relevant will be the comparability and

accuracy of national fiscal and

macroeconomic statistics.

Significant evidence of „creative“ accounting

Large heterogeneity of fiscal accounting

approaches in EU

Conclusions

22

Thank you for your attention!

References:

Darvas, Zsolt and Àlvaro Leandro (2015). ‘The limitations of policy coordination in the

euro area under the European Semester’. Bruegel Policy Contribution. 2015/19

IMF (2013). ‘Towards a Fiscal Union for the Euro Area:Technical Background Notes’.

Von Hagen, Jürgen and Guntram B. Wolff (2004). ‘What do deficits tell us about

debt? Empirical Evidence on creative accounting with fiscal rules in the EU’.

Discussion paper No 38/2004. Deutsche Bundesbank.

Guntram.Wolff@bruegel.org