WP/16/172

Negative Interest Rate Policy (NIRP):

Implications for Monetary Transmission and Bank

Profitability in the Euro Area

by Andreas (Andy) Jobst and Huidan Lin

IMF Working Papers describe research in progress by the author(s) and are published

to elicit comments and to encourage debate. The views expressed in IMF Working

Papers are those of the author(s) and do not necessarily represent the views of the IMF, its

Executive Board, or IMF management.

©2016 International Monetary Fund WP/16/172

IMF Working Paper

European Department

Negative Interest Rate Policy (NIRP):

Implications for Monetary Transmission and Bank Profitability in the Euro Area

Prepared by Andreas (Andy) Jobst and Huidan Lin

1

Authorized for distribution by Mahmood Pradhan

August 2016

Abstract

More than two years ago the European Central Bank (ECB) adopted a negative interest rate

policy (NIRP) to achieve its price stability objective. Negative interest rates have so far

supported easier financial conditions and contributed to a modest expansion in credit,

demonstrating that the zero lower bound is less binding than previously thought. However,

interest rate cuts also weigh on bank profitability. Substantial rate cuts may at some point

outweigh the benefits from higher asset values and stronger aggregate demand. Further

monetary accommodation may need to rely more on credit easing and an expansion of the

ECB’s balance sheet rather than substantial additional reductions in the policy rate.

JEL Classification Numbers: E43, E52, E58, G21

Keywords: negative rates, NIRP, unconventional monetary policy, monetary transmission

Author’s E-Mail Address: [email protected]; [email protected]

1

The paper also includes contributions from Jiaqian (Jack) Chen, Jesse Siminitz, and Rima Turk. We thank Shekhar Aiyar,

Craig Beaumont, Kelly Eckhold, Rachelle van Elkan, Jennifer Elliott, Kevin Fletcher, Gee Hee Hong, Diarmuid Murphy,

Phakawa Jeasakul, Kenneth Kang, Erik Lundback, Borislava Mircheva, Jasmina Mrkonja, Machiko Narita, Jean-Marc

Natal, Hiroko Oura, Marcel Peter, Mahmood Pradhan, Tove Katrine Sand, Damiano Sandri, Louise Funch Soerensen, Yan

Sun, Tomohiro Tsuden, Rima Turk, Niklas Westelius, and Johannes Wiegand for helpful comments and suggestions. We are

also grateful to staff from the Directorate Monetary Policy and the Directorate General Macro-Prudential Policy and

Financial Stability at the European Central Bank (ECB) for their feedback. A shorter version of this paper was published as

Selected Issues Paper (Jobst and Lin, 2016) in the context of the 2016 Article IV Consultation with the Euro Area.

IMF Working Papers describe research in progress by the author(s) and are

published to elicit comments and to encourage debate. The views expressed in IMF

Working Papers are those of the author(s) and do not necessarily represent the views of

the IMF, its Executive Board, or IMF management.

Contents Page

I. Introduction ............................................................................................................................4

II. Arguments Surrounding NIRP ..............................................................................................7

III. The Impact of Negative Interest Rates ...............................................................................13

IV. Assessment for the Euro Area ...........................................................................................20

V. Conclusion ..........................................................................................................................27

References ................................................................................................................................29

Tables

1. Overview of Central Banks with Negative Policy Rates .......................................................6

Figures

1. Deposit and Lending Rates (New Lending) for Households ...............................................16

2. Marginal Policy Rate (Central Bank Deposit Rate) and Bank Net Interest Margin ............17

3. Currency in Circulation and Pervasiveness of Negative Interest Rates ...............................20

4. The Impact of NIRP on Bank Profitability and Implications for Credit Growth ................25

5. Bank Equity Valuation and Credit Growth ..........................................................................26

Boxes

1. The Mechanics of Tiered Reserve Systems .........................................................................10

2. Reducing the Direct Cost of NIRP and the Role of Tiering in Monetary Transmission .....14

Appendices

I. Implementation Issues under NIRP ......................................................................................35

II. Overview of Other Countries with NIRP ............................................................................41

III. Monetary Conditions in Countries with NIRP ...................................................................44

4

I. INTRODUCTION

Since the 1990s interest rates have been declining and remain low across all major advanced

economies. In particular, low long-term interest rates reflect the diminishing return on safe

assets due to demographic changes, a slowdown in the rate of technological progress, and a high

demand for safe assets relative to their supply (Bean and others, 2015). Given the secular

decline of inflation and inflation expectations and short-term policy rates approaching zero

percent, this has made it more difficult for accommodative monetary policies to reduce real

interest rates to a level consistent with stable inflation and output at its potential level

(technically, the “natural” rate of interest). For a long time, central bankers believed that the

policy rate could not drop below zero, because households and corporates might start converting

deposits into cash to avoid devaluation−thus, conflating the nominal lower bound with the

“physical lower bound”. However, not going below zero percent meant that with inflation

remaining low, real rates could not fall further to help reduce high debt burdens and support

aggregate demand.

More than two years ago, following the example of the Danmarks Nationalbank (DN), the

European Central Bank (ECB) became the first major central bank to effectively move its

marginal policy rate into negative territory in response to these macroeconomic challenges. The

move in June 2014 strengthened its forward guidance about the expected future path of interest

rates and complemented a series of further easing measures aimed at bringing inflation back to

-0.5

-0.3

-0.1

0.1

0.3

0.5

0.7

2010 2011 2012 2013 2014 2015 2016

Major Reserve Currencies: Effective

Marginal Policy Rates, 2010-2016

(Percent)

Euro area

United States

UK

Japan

Sou rce: Bloomberg, L.P.; and Haver An alytics.

Note: Policy rates used for each country are the following: EA:

deposit rate; US: Fed funds rate; UK: O/N interbank rate; Japan:

deposit rate.

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

-1.0

-0.5

0.0

0.5

1.0

1.5

2010 2011 2012 2013 2014 2015 2016

Other Currencies: Effective Marginal

Policy Rates, 2010-2016

(Percent)

Sweden

Denmark

Bulgaria

Switzerland

Hungary (rhs)

Sou rce: Bloomberg, L.P.; and Haver Analytics.

Note: Policy rates used for each country are the following: SWE:

reverse repo rate; DEN: certificates of deposit rate; HUN: deposit

rate; BGR: deposit rate; CHE: deposit rate.

5

the ECB’s price stability objective of below, but close to, two percent over the medium term.

Also other central banks−the Sveriges Riksbank (SR) and the Swiss National Bank (SNB)−cut

their marginal policy rates to below zero percent over the period from mid-2014 to early 2015

(see text figures).

2

Central banks in Norway (September 2015), Japan

3

(February 2016), and

Hungary (March 2016) lowered only their deposit rate for excess bank reserves while keeping

the main policy rate in positive territory.

4

While some central banks have adopted a negative

interest rate policy (NIRP) to counter low inflation (ECB, BoJ, SR),

5

others have focused on

mitigating spillover effects from unconventional monetary policy (UMP) measures (Mircheva

and others, 2016) and to address currency appreciation pressures (DN, SNB) (Table 1 and

Appendix I, Table A1). Most central banks have also introduced a tiered deposit rate to reduce

banks’ cost of holding excess reserves while still allowing for a strong pass-through to money

markets (Appendix II).

2

DN cut its policy rate to below zero in July 2012 and the rate stayed negative until April 2014. It turned negative for a second

time in September 2014.

3

The interest rate on excess reserves is technically not the key policy rate in Japan. The complementary deposit facility was

introduced at the end of October 2008 to ensure stability in financial markets.

4

Both Hungary and Norway are not true cases of NIRP and are included for completeness only. While the Magyar Nemzeti

Bank (MNB) used negative rates to promote new lending and reduce vulnerabilities, in particular regarding public debt, no

liquidity is effectively priced at the negative deposit rate in Hungary, and the MNB offers fixed rate full allotment at three-month

deposit auctions each week at the (positive) policy rate. In the case of Norway, the negative reserve rate is not a policy measure

but part of normal liquidity operations to motivate banks to lend reserves to other banks rather than deposit them with Norges

Bank (NB). Like in Hungary, the key policy rate remains positive, and the negative deposit has had little or no influence on the

money market (NOWA) rate. In absence of excess reserves above a certain quota (“reserve rate”), the cost of holding reserves

rather than lending them to other banks is the same as when the reserve rate was positive.

5

In Sweden, policymakers undertook domestic UMP including negative policy interest rates in order to address low inflation

and a sharp decline in inflation expectations; this also help avoid deflationary pressures from the exchange rate pass-through in

an inflation-targeting regime. The effect of this package was to keep the Swedish bond yields broadly aligned with those on

German Bunds even as the latter yields fell owing to the ECB’s UMP. The Swedish krona remained broadly stable against the

euro, avoiding an appreciation that could have significantly hindered the SR’s efforts to return inflation to its target.

6

Table 1. Overview of Central Banks with Negative Policy Rates

Policy Rates (in basis points) 1/

FX regime

Objective

Overnight

Lending 2/

Open Market

Operations

Deposit

Facility

Date of

Introduction

Denmark

Conventional peg

(to euro)

Countering safe-

haven inflows and

exchange rate

pressures

5 0

-65

July 2012-

April 2014,

Sept. 2014

Euro Area

Free floating,

inflation-targeting

framework

Price stability and

anchoring inflation

expectations

25 0

-40 June 11, 2014

Hungary

Floating, inflation-

targeting

framework

Price stability and

countering

exchange rate

pressures

115

90 -5 March 23, 2014

Japan

Free floating,

inflation-targeting

framework

Price stability and

anchoring inflation

expectations

10 0

-10 Feb. 16, 2016

Norway

Free floating,

inflation-targeting

framework

Price stability 3/ 150

50 -50 Sept. 24, 2015

Sweden

Free floating,

inflation-targeting

framework

Price stability and

anchoring inflation

expectations

25

-50 -125 Feb. 12, 2015

Switzerland

Free floating 4/

Reducing

appreciation and

deflationary

pressures 5/

50 n.a.

-75 Jan. 15, 2015

Source: National central banks and authors. Note: 1/ effective policy rate are highlighted with a red background, as of end-July 2016; 2/ refers to

special rate (liquidity-shortage financing facility) in the case of Switzerland; 3/ Norway has not adopted NIRP, and the negative interest rate on bank

deposits at the central bank (“reserve rate”) has had little or no influence on market rates. The reserve rate is one percentage point below the sight

deposit rate (key policy rate). On average, NB has kept reserves in the banking system at around NOK 35 billion (and below the aggregate quota of

NOK 45 billion). Thus, a bank with reserves in excess of the quota will always be able to deposit reserves with a bank with room on its quota.; 4/

conventional peg (to euro) before January 15, 2015); 5/ in conjunction with the exit from the exchange rate ceiling.

7

II. ARGUMENTS SURROUNDING NIRP

In an environment of low inflation and a declining equilibrium real rate of interest, negative

rates restore the signaling capacity of the central bank by effectively removing the zero lower

bound (ZLB). Moving the marginal policy rate into negative territory can help the real rate

adjust downward, compensating for inflation below the inflation target (text figure) and

contributing to a significant flattening

of the yield curve.

6

In other words, a

decline in the nominal rate could lower

its real rate component, allowing

inflation expectations to rise and

boosting aggregate demand; however, if

both nominal and real interest rates are

shifted down, a widening gap leads to

deflation pressure.

7

Thus, if banks hold

excess reserves, cuts to the central bank

deposit rate (as the marginal policy

rate) can effectively lower the interbank

and other interest rates, encouraging

banks to take greater risks and

facilitating portfolio rebalancing.

Assessing the effect of NIRP on

exchange rates is difficult since many other factors influence external demand. Negative rates

cause exchange rates to depreciate by providing incentives for moving capital to higher-yield

jurisdictions. Thus, a widening real term spread differential would put downward pressure on

the currency. Higher inflation and inflation expectations in other countries might counter this

effect. In addition, the stimulative effect of negative rates on aggregate demand (which is

discussed below) and rising asset prices in real terms might offset depreciation pressures on the

exchange rate.

6

Already subdued interest rate expectations limit any additional support provided by forward guidance on policy rates, with

slowing growth challenging the credibility of commitments to anchor inflation expectations.

7

The nominal interest rates can be decomposed into two components, the real rate and expected inflation.

-2

-1

0

1

2

3

4

5

6

7

8

-2 0 2 4

Nominal Interest Rate/

Effective Policy Rate

Core CPI Inflation Rate

US

UK

Japan

Euro Area

Inflation and Interest Rates, Jan. 2002-April 2016

(Inpercent, monthly)

Source: Bloomberg, Haver Analytics, and IMF staff calculations.

Non-linear

Taylor Rule for

Inflation Target

of 2%

Fisher

Relation

i = natural

rate + x

Deflation

Equilibrium

8

The economic lower bound of NIRP is largely determined by the impact of negative rates on

financial intermediation. While there is some direct cost pressure from charging interest for

excess liquidity that banks hold at the central bank (suggesting limits to negative rates based on

the tendency of banks to raise cash balances), some central banks have implemented mitigating

policy to limit the incentive to move into cash—such as tiered reserve regimes and penalties for

banks making large transfers of reserves into cash. As rates become more negative, the lower

nominal bound is increasingly determined by the broader indirect pressure coming from

diminishing bank profitability as most lending rates are assumed to fall more than deposit rates.

The downward stickiness of deposit rates could result in a difficult trade-off between effective

monetary transmission and bank profitability. If negative policy rates are transmitted to lower

lending rates (and term premia),

8

banks are likely to see their interest earnings decline unless

they either impose negative rates (or commensurate fees) on deposits or substitute more

wholesale funding (at lower money market rates) for deposits.

9

But retail deposit rates tend to be

downward sticky since (i) households and small businesses do not face the same set-up cost as

banks and corporations in storing cash,

10

and (ii) a zero percent interest rate could be a

psychological threshold (Alsterlind, 2015).

11

The stickiness of deposit rates reflects the

avoidance of being penalized to save and is determined by the actual costs of holding cash rather

than deposits; under these conditions, demand for cash is likely to be greatest for economic

agents with high excess liquidity and increases if negative interest rates are expected to persist

for some time.

12

As a result, banks’ net interest margins (NIMs), defined as net interest income

8

In addition, in countries with a high share of variable rate lending (and/or indirect pressure on bank lending rates from

corporate bond markets), the impact of negative rates on the re-pricing of existing loans is likely to outweigh the profits from

new lending.

9

While deposits tend to represent the major source of funding for most banks, some also rely on funding via unsecured bonds,

covered bonds, and securitization, which are likely to be more responsive to changes in interest rates than deposits. Banks could

substitute wholesale funding for more expensive retail deposits (also to meet stable funding requirements under the Basel

liquidity risk framework); however, longer-term funding contains some term premium, and market access might be limited for

smaller banks, especially in countries where banks rely heavily on deposit funding.

10

The costs of holding cash rather than deposits can be calculated by adding up the costs for secure storage and transport, as

well as for settling payments in cash, which is likely to be small for households and small businesses.

11

For example, compared to more sophisticated agents, households may simply react more instinctively to negative rates

viewing negative rates as “abnormal” or “theft.”

12

If banks eventually decide to lower retail deposit rates below zero as done on large deposits in several countries, this would

increase the chances of “leakages” to cash. This can be gauged from consumers’ cash preference in retail transactions. Despite

the higher social cost of settling cash payments (i.e., costs incurred by the financial sector, retailers and households), empirical

evidence suggests that consumers have a strong cash preference to avoid potential fees on electronic payments. For example, in

early 2005, Danish banks and retailers were allowed to pass on part of the costs of electronic transactions to consumers, which

is—for each marginal unit of money spent—economically equivalent to imposing negative rates on savings; this move caused

9

relative to average interest-earning assets, compress as lending rates for new loans decline and

existing (variable-rate) loans re-price while deposit rates remain sticky. This could reduce bank

profitability and impair the pass-through to lending rates.

13

Thus, banks might also consider

increasing lending rates if they face (i) a considerable opportunity cost of accepting deposits at

non-negative rates as wholesale funding costs decline in lock-step with the marginal policy rate

and/or (ii) corporate deposit rates cannot be cut to potentially subsidize sticky retail deposit

rates.

A prolonged period of negative rates could also raise financial stability concerns. In particular,

the downward stickiness of deposit rates encourages banks to substitute less stable wholesale

funding for deposits. For example, German, Italian, Portuguese, and Spanish banks, whose

deposit base is wider than the euro area average, would have stronger incentives to trade off

market-based sources of funding against more stable (term) deposit funding (Figure 3). This

calls for greater emphasis on the appropriate supervision of bank liquidity, including the

transition to the liquidity coverage ratio (LCR) and net stable funding ratio (NSFR)

requirements.

As much as negative rates ease financial constraints on borrowers in the short run, they could

distort the long-term debt affordability for borrowers if lending rates become negative in real

terms.

14

The reduced debt service burden under NIRP could delay the exit of nonviable firms,

hurting demand prospects of healthy firms by adding to excess capacity and delaying the

efficient allocation of capital and labor (Caballero and others, 2008; Kwon and others, 2015).

15

By effectively removing the profitability constraint of investments as real borrowing rates drop

to or even fall below the ZLB, NIRP might also delay corporate restructuring in countries with

debt overhangs, especially if inflation does not pick up. In these instances, more assertive

supervision and regulatory pressures would be needed to address large amounts of non-

performing loans and debt overhang problems (Syed and others, 2009).

the number of transactions to drop sharply (Abildgren and others, 2010), suggesting that the lowest socially acceptable deposit

rate might not be far below the ZLB.

13

For a comprehensive analysis of how cash hoarding can be prevented under NIRP, see Agarwal and Kimball (2015).

14

This would necessitate a tightening of lending standards if greater risk-taking due to NIRP undermines the usefulness of asset

impairment levels in detecting financial distress.

10

Box 1. Monetary Transmission under NIRP

1

We assess the impact of negative rates on bank profitability and its implications for monetary transmission when

deposit rates become sticky using a general equilibrium specification. We adapt the DSGE model by Gerali and

others (2010), which was estimated using euro area data. In the model, banks enjoy monopoly powers in

intermediating funds between savers and borrowers and setting rates on loans and deposits. The modeled banking

sector comprises two retail branches, which are responsible for lending and deposit-taking, while the wholesale unit

manages the capital position of the banking group subject to a simple solvency constraint, and, in addition, provides

wholesale loans and raises wholesale funding. Banks face different adjustment costs when changing rates. A higher

cost implies lower adjustment for a given shock, and, thus, the rates are more “sticky.”

Source: authors. Note: blue line=unchanged pass-through scenario (first scenario, base case); green dotted line=sticky deposit

scenario but non-binding solvency constraint for banks (second scenario); red line= sticky deposit scenario and binding solvency

constraint for banks (third scenario).

11

Box 1. Monetary Transmission under NIRP

(Concluded)

Sticky deposits under NIRP seem to either weaken bank profitability or diminish monetary transmission. We

examine three different scenarios reflecting banks’ response to a policy rate cut assuming that deposit rates are

bounded at zero percent (text chart below). Banks can substitute some cheaper wholesale funding for deposit

funding but potentially offsetting components of banks’ net operating income are ignored (e.g., capital gains from

higher asset prices and lower provisioning cost from higher debt service capacity of borrowers). While higher asset

prices boost the investment income, lower funding costs, and decrease provisioning expenses of euro area banks,

these benefits weaken over time relative to the adverse effect of compressed interest margins where the pass-

through of policy rates is high and credit demand is low.

In the first case (blue line), we assume that the pass-through from the policy rate to deposit rate remains unchanged.

Banks reduce the both deposit and lending rates, and their profitability increases over time as output and inflation

outturns improve. In the second case (green dotted line), price-setting banks face (artificially) higher adjustment

costs in setting deposit rates (i.e., deposits are “sticky”). Banks optimally choose to lower lending rates to increase

lending volume at the cost of deviating temporarily from the minimum capital requirement (Angelini and others,

2014). Bank profitability declines significantly as lending volumes are initially insufficient to offset the

compression of lending margins due to sticky deposit rates. In the third case (red line), banks’ solvency constraint

is strictly enforced for the second scenario of sticky deposits. Here, monetary transmission breaks down as banks

(initially) increase lending rates and curtail credit growth given the limited substitution of wholesale funding (due to

a large deposit base). However, the impact on output is still positive, although smaller over the short term, as the

wealth and substitution effects (from lower discount rates) pushes up loan demand, supporting consumption and

investment. In general, the simulation results suggest a positive aggregate impact of NIRP under all three scenarios

but rising pressures on bank profitability over the short and medium terms if deposit rates have reached a lower

bound and banks are capital-constrained.

1

Prepared by Jiaqian (Jack) Chen and Andreas (Andy) Jobst.

Negative rates also have distributional implications that are beyond the scope of this paper. For

instance, negative rates could increase the re-distributional impact of monetary policy on wealth

and income. Any reduction in interest rates makes savers worse off while borrowers benefit and

could have important intergenerational implications. Elderly people tend to have accumulated

savings, so moving from positive to negative interest rates could increase intergenerational

inequality as retirement income declines. However, higher asset prices increase the net worth in

present value terms. Lower borrowing rates also support consumption and investment of

liquidity constrained households and firms, raising aggregate demand over time and

outweighing any adverse impact on savings.

However, several important factors could compensate for the adverse impact of NIRP:

Stronger credit growth and/or higher non-interest income. The credit supply effects of

reduced profitability from lower lending rates can be offset by the credit demand effects if

banks increase lending (Box 1)—but this becomes more difficult if credit demand is low,

12

assets re-price quickly, and competition among banks is high. Banks could also

supplement declining interest margins with alternative sources of income, such as fees

and commissions.

16

Higher asset prices and lower funding costs. Portfolio rebalancing with negative rates

reduces term and credit risk premia, eases financial conditions and ultimately supports

credit creation and economic activity. The resulting decline in risk aversion increases

asset prices and generates capital gains for banks. Furthermore, higher asset prices

(especially in tandem with higher inflation) are likely to raise future income and

strengthen borrowers’ repayment capacity, lowering banks’ expected provisioning costs

and write-off charges for non-performing loans (NPLs).

17

Stronger aggregate demand through portfolio rebalancing. Negative rates also increase

household consumption and steer portfolio rebalancing towards other investment

opportunities, with beneficial effects on aggregate demand.

18

Portfolio rebalancing helps

lower firms’ general cost of capital via lower term premia on corporate bond yields.

19

At a

lower cost, more investment projects would become profitable, raising investment and

credit demand. Higher asset prices and lower interest expenses for indebted households

(who tend to have higher marginal propensity to consume) also boost household

consumption through wealth effects.

20

16

For instance, charging retail clients fees to maintain checking accounts as it is done commonly in the United States.

17

Bolt and others (2012) find a strong impact of output growth on bank profitability, with loan losses as the main driver.

18

Thus, the “true” limit on negative deposit rates would be the level at which households would find it preferable to hoard large

amounts of cash. Given the costs of moving and storing cash, this rate can be well below zero.

19

Even though the portfolio rebalancing channel would apply to any reduction of policy rates, its effectiveness might change in

an environment of negative interest rates depending on how lower risk aversion affects investment behavior. Greater risk taking

via the portfolio rebalancing under NIRP also implies that some safe assets, such as government bonds, will yield negative

returns (depending on the maturity term), and, thus, represent a guaranteed loss of purchasing power if held to maturity. As safe

assets are being removed from the financial system and replaced with riskier assets, some investors will take more risk to

compensate for loss of income while others might be forced to reduce their risk exposure in response. In addition, regulatory

requirements, including capital adequacy considerations, can affect the portfolio rebalancing channel (Berkmen and Jobst,

2015).

20

For example, Genay and Podjasek (2014) find that the estimated negative effect on bank profits of low interest rate

environment is small and outweighed by the likely positive effects on profits of low interest rates boosting economic activity.

13

III. THE IMPACT OF NEGATIVE INTEREST RATES

Overall financial conditions have improved as central banks in many advanced economies set

policy rates at record low levels, without causing significant swings in exchange rates. Negative

rates have been fairly effective thus far in reducing money market rates and have been

transmitted to the wider economy through lower lending rates for both corporates and

households as lending standards have eased (Elliott and others, 2016; Viñals and others, 2016).

At the same time, retail and corporate deposit rates also have declined, allowing most banks to

maintain their lending margins and supporting credit growth.

21

In cases where sticky deposits

have compressed lending margins, banks have shifted some of their activities to fee-based

services and/or increased their lending volumes to offset declining interest revenues. Negative

rates have so far had a muted impact on exchange rates as current disinflationary dynamics in

many countries with negative rates prevent real rates from declining further (see text figures).

Money market rates have closely followed an increasingly negative marginal policy rate without

disruptions to market functioning (Appendix III, Figures A1 and A2). In the environment of

excess liquidity, the observed money market rate will be at or just above the marginal policy rate

at which excess reserves are remunerated (or penalized under NIRP).

22

In several countries, a

tiered central bank deposit rate has facilitated the smooth transmission of the marginal policy

rate to money markets, reducing the cost of interbank lending and restoring the signaling

capacity of the central bank and strengthened its commitment to keep rates low for an extended

21

See McAndrews (2015) for a critical review of issues concerning negative interest rates.

22

Banks would be willing to lend at rates above the negative deposit rate but there are no (or very few) borrowers given excess

reserves in the system, and, thus, the overnight money market rate converges to the deposit rate.

95

100

105

110

115

120

125

Exchange Rates relative to Euro

(Index, time t = 100, day before introduction of

negative deposit rates)

Sweden Denmark

Switzerland Japan

Hungary Bulgaria

Source: Haver Analytics. Note: the x-axis shows monthly intervals.

75

80

85

90

95

100

105

110

115

120

125

Exchange Rates relative to U.S. Dollar

(Index, time t=100, day before introduction of

negative deposit rates)

Sweden Denmark

Switzerland Japan

Hungary Bulgaria

Euro

Source: Haver Analytics. Note: the x-axis shows monthly intervals.

14

period of time (Box 2). However, several factors, in particular related to the design of a tiered

reserve system, could keep the money market rate away from the deposit rate as the technical

floor of the policy rate corridor (Appendix I, Box A1). These include: (i) the amount of excess

liquidity and the fraction that is exempted from the marginal policy rate, (ii) the spread between

the marginal and average policy rate for excess reserves, and (iii) banks’ willingness/ability to

lend excess liquidity to each other (fragmentation).

Box 2. Reducing the Direct Cost of NIRP and the Role of Tiering in Monetary Transmission

The implementation of a second effective deposit rate for excess reserves (such as through tiering) would increase

the central bank’s general capacity to pursue NIRP while mitigating the direct cost to banks. More specifically,

excess reserves can be held in both the current account and the deposit facility of central banks. In a tiered regime,

the exemption typically applies to the current account (which satisfies the minimum reserve requirement); thus,

banks would have an incentive to shift excess reserves from the deposit facility to the current account to reduce the

cost of negative rates up to a certain limit. Currently, euro area banks’ overnight deposits (€297 billion) and current

account balances (€613 billion) amount to about €910 billion. The minimum reserve requirement of €116 billion is

remunerated at the MRO rate of 0 percent, which leaves excess reserves of €794 billion subject to the negative

deposit rate of -0.4 percent as the marginal policy rate—setting the lowest rate at which banks would be prepared to

lend to each other (which is reflected in the theoretical EONIA rate in the chart below). Thus, the direct (annual)

cost of negative rates (without

implementation of a tiered

reserve regime) is about €3.2

billion for all euro area banks

in aggregate (and 0.1 percent

of total consolidated assets).

In other words, a 10 basis

point reduction in the deposit

rate results in a direct cost of

about €0.8 billion per year.

Given the recent experience in

Switzerland, where the direct

cost of NIRP did not exceed

0.03 percent of total assets

(Barr and others, 2016),

1

the

current deposit rate may have

already reached its limit

(without considering any

mitigating effects). However,

for a tiered reserve regime

excluding 75 percent

2

of

excess reserves from the

negative deposit rate (in line

with reserve system in

Switzerland), the Eurosystem

could theoretically tolerate

further cuts to the deposit rate

based on the direct cost of

NIRP only.

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

MRO

Deposit facility

EONIA (O/N)

Volume-weighted average GC repo 1/

Euro Area: EONIA and Repo Rates

(percent)

Source: Bloomberg L.P., ECB, and IMF staff calculations. Note: 1/

Composite of German, French and Italian GC repo.

0

200

400

600

800

1,000

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

Deposit facility

EONIA (O/N)

Theoretical EONIA (O/N) 1/

Excess liquidity (rhs)

Euro Area: Actual and Theoretical EONIA Rate

(percent/EUR billion)

Source: Bloomberg L.P., ECB, and IMF staff calculations. Note: 1/

The theoretical EONIA rate is calculated as the average of the MRO

and deposit rate, weighted by the relative proportion of the ECB's

current account balance and excess reserves.

150

160

170

180

190

200

5

10

15

20

25

30

35

40

Sep-13

Dec-13

Mar-14

Jun-14

Sep-14

Dec-14

Mar-15

Jun-15

Sep-15

Dec-15

Mar-16

Jun-16

Unsecured (EONIA O/N) 1/

Repo market (govt. debt), rhs 2/

Euro Area: Secured and Unsecured Lending

Volumes (EUR billion)

Source: Bloomberg L.P., ECB, and IMF staff calculations. Note: 1/

trading volume of overnight contracts; 2/ composite outstanding

volume of general collateral (GC) repo on German, French, and

Italian government debt.

negative

rates

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Jan-13

Apr-13

Jul-13

Oct-13

Jan-14

Apr-14

Jul-14

Oct-14

Jan-15

Apr-15

Jul-15

Oct-15

Jan-16

Apr-16

MRO

Deposit facility

EONIA (3-month)

Bank certificate of deposit (3-month)

Euro Area: EONIA and Certificate of Deposit

Rate (percent)

Source: Bloomberg L.P., ECB, and IMF staff calculations.

15

Box 2. Reducing the Direct Cost of NIRP and the Role of Tiering in Monetary Transmission

(Concluded)

The direct cost of a negative deposit rate on excess reserves is relatively small, even without tiering, but affects

banks disproportionately due to significant differences in excess reserve holdings. Since the ECB charges interest

only on excess liquidity, the charge is greater in those countries where banks hold large excess reserves. These are

generally countries with substantial current account surpluses vis-à-vis other members of the monetary union.

Banks in other economies hold much lower excess reserves and thus are much less affected.

In comparison, the indirect effect of NIRP via (potentially) lower bank profitability from lending can be large.

Given a total outstanding amount of loans of about €17.6 trillion (end-May 2016) at an average interest spread of

0.8 percent, euro area banks would record aggregate net interest income of about €141 billion (gross of operating

expenses, provisioning, and taxes). Based on a (historically conservative) pass-through of 50 percent, a 10 basis

point rate cut would reduce lending margins by 5 basis points and result in an indirect cost of about €8.8 billion (or

11 times the estimated direct cost of NIRP above). Valuation gains from investments and trading income might, to

some extent, mitigate these costs. However, the aggregate balance sheet of euro area banks suggests that lending is

about 6-7 times more important than investments for profitability.

Fine-tuning the exempted portion of excess reserves can alter the effective monetary transmission of negative rates

to money markets. In its current reserve regime, the ECB achieves negative short-term money market rates by

setting a positive policy rate (MRO at 0 percent) and a negative interest rate on the deposit facility (-0.4 percent)

while maintaining excess reserves in the banking system. The money market rate is pushed down towards the

lowest marginal policy rate because banks will try to lend their surplus liquidity to other banks in the interbank

market to avoid using the central bank’s deposit facility—but only as long as the lending rate exceeds the deposit

rate.

3

Given the prevailing excess liquidity in the system, the overnight money market rate (EONIA) has converged

to the volume-weighted average of (i) the deposit rate (at -0.4 percent) for excess reserves and (ii) the marginal

refinancing operations (MRO) rate (of 0 percent), which applies to banks’ minimum reserve requirement held in the

ECB’s current account (see text chart above). Thus, the transmission of the marginal policy rate is also affected by

the dispersion of the excess liquidity among banks and banks’ willingness/ability to lend excess liquidity to other

banks.

4

This also holds true for secured funding markets (repo), where rates have similarly adjusted downward as

the ECB lowered the deposit rate (see text chart). The experience in countries with tiered deposit rates shows that

the average rate has a large impact on the fixing; thus, a volume-weighted average of potentially two deposit rates—

by excluding a certain share of reserves from the deposit rate and removing some excess liquidity from interbank

market—below the marginal policy rate could marginally push up the money market rate.

The effective transmission of the policy rate can also be assessed based on the sensitivity of unsecured term funding

of banks via certificates of deposits (CDs). The CD rate reflects the willingness of money market funds to lend to

issuing banks over a pre-defined maturity term (see text chart). Since the CD rate continues to track the marginal

policy rate very closely even under NIRP (without a change in volumes), this suggests that banks are able to impose

lower and negative rates on investors despite counterparty risk given the unsecured nature of CDs.

_______________________________

1

The assumption of exempting 75 percent of reserves from a negative deposit rate was based on the experience in Switzerland

where the share of the overall reserve stock subject to negative deposit rates averaged 23 percent until end-2015. In practice,

given the significant heterogeneity of bank business models, banks’ tolerance threshold for the direct cost of negative rates might

be different in the euro area than in Switzerland.

2

The exemption of a certain amount of reserves can vary over time (and would need to decrease as excess liquidity declines).

The opportunity cost of lending can be increased (on average) by calibrating the tiering such that the price of depositing cash

with the ECB would be the same (or higher) than the expected net interest margin from lending multiplied by the share of the

deposit base funding loans (i.e., the inverse of the aggregate loan-to-deposit ratio of the banking sector).

3

The money market rate could be higher than the lowest marginal policy rate if the exempted portion of excess reserves is too

large, leaving banks little incentive to engage in interbank lending; thus, lower supply of liquidity could create potential scarcity

in some parts of the system, pushing up money market rates above the technical floor of the ECB deposit rate.

4

Given that the average daily quoted turnover underpinning EONIA fixings has only been about €12.6 billion (or 1.5 percent of

excess liquidity) since January 2016, the impact of the marginal policy rate on money market rates is quite sensitive to changes

in bank behavior and rate setting.

16

Figure 1. Deposit and Lending Rates (New Lending) for Households

(January 2005–June 2016, percent)

Negative policy rates also have been transmitted to the wider economy through lower lending

rates for both corporates and households as lending standards have eased. In most countries,

banks lowered their lending rates to both households and firms (which continued to decline even

as deposit rates had reached the ZLB) while offsetting the negative impact on lending margins

(when deposit rates adjusted less) by some small increase in fees and commissions and cost

cutting. However, this has occurred, in most cases, as long as deposit rates still had some room

to drop to the ZLB (see text figures and Figure 1), allowing banks to transmit lower policy rates

2

3

4

5

6

7

0123456

since July 2014

until June 2014

Deposit Rate

Lending Rate

Euro Area

3

4

5

6

7

8

9

0123456

since July 2014

until June 2014

Deposit Rate

Lending Rate

Denmark

1

2

3

4

5

6

7

012345

since July 2014

until June 2014

Deposit Rate

Lending Rate

Sweden

Source: Bloomberg L.P., Haver and IMF staff calculations.

2

2.5

3

3.5

4

0 0.1 0.2 0.3

since July 2014

until June 2014

Deposit Rate

Lending Rate

Switzerland

17

without impeding their profitability (Box 1).

23

In some countries (e.g., Denmark and Sweden),

banks also passed negative rates to deposits of some large corporations and institutional

investors but maintained positive rates for retail depositors. In Switzerland, lending rates

adjusted only slowly when policy rates moved into negative territory, helping to raise bank

profitability (Appendix III, Figure A3).

Figure 2. Marginal Policy Rate (Central Bank Deposit Rate) and Bank Net Interest

Margin (January 2010–May 2016, percent)

23

Whether this effect is stronger or weaker at negative rates remains unclear. Claessens and others (2016) suggest that interest

rate cuts reduce banks’ NIMs, and this effect increases the lower the policy rate.

1.10

1.15

1.20

1.25

1.30

-1.0 -0.5 0.0 0.5 1.0 1.5

Net interest margin

Deposit rate (percent)

Denmark

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

-1.0 -0.5 0.0 0.5 1.0 1.5

Net interest margin

Deposit rate (percent)

Sweden

Source: Bloomberg, L.P.; Haver Analytics.

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

-0.5 0.0 0.5 1.0

Net interest margin

Deposit rate (percent)

Euro Area

0.6

0.7

0.8

0.9

1.0

1.1

1.2

1.3

1.4

1.5

-1 -0.5 0 0.5

Net interest margin

Deposit rate (percent)

Switzerland

18

The direct cost imposed on excess bank reserves is modest relative to the size of the overall

balance sheet. Negative rates have important implications for banks’ cost of holding central

bank liabilities depending on the structure of reserves and their remuneration (Appendix I,

Box A1) and the transmission of the marginal policy rate to money markets. However, bank

profitability is far less sensitive to negative

rates on excess reserves (even under a tiered

system) since cash balances of banks represent

only a fraction of their asset base (although

there are significant differences in the

distribution of reserves around the euro area).

That said, many banks earn negative returns

on many liquid assets, which are required for

liquidity risk management and represent a

significant portion of their balance sheet. At

the same time, rolling over these short-term

holdings tends to offset any benefits from

valuation gains.

In the euro area and countries with an even more negative deposit rate (Denmark, Sweden and

Switzerland), there have been no clear signs of cash hoarding (see text figure).

24

Current levels

of negative rates seem to provide insufficient incentives to build alternative storage capacity for

excess reserves. However, banks have been hesitant to pass on negative rates to depositors—

with the exception of large corporates (e.g., Denmark and Switzerland)—limiting the incentives

for hoarding cash. In fact, most of the recent increase in cash holding in some countries

(Denmark and Switzerland) can be explained by the normal relation between currency in

circulation and movements in the short-term interest rate, reflecting the reduced opportunity cost

of holding cash rather than deposits (Figure 3). Irrespective of whether interest rates are positive

or negative, the amount of currency in circulation increases when interest rates decline.

25

Despite lower lending rates, there is limited evidence so far of negative rates having directly

damaged bank profitability; however, they have contributed to the flattening of the yield curve.

24

In the case of Switzerland, the annual growth of currency in circulation is now higher than the pre-NIRP period (especially

high-denomination banknotes). However, currency growth rates are still below those observed in earlier years (e.g. 2009 and

2012).

25

The avoidance of negative deposit rates by corporates can also affect other parts of the economy. For instance, Danish tax

authorities had to restrict the amount of taxes firms could prepay in order to receive modest interest on the deposits, which are

credited against what they owe or are refunded, and, thus, limiting the use of tax collection as a quasi-bank account to avoid

negative interest rates on taxable income (Campbell and Levring, 2016).

-20

-15

-10

-5

0

5

10

15

20

t-3 t-1 t+1 t+3 t+5 t+7 t+9

Currency in Circulation at Time of Negative

Deposit Rates

(Percent, year-on-year)

Euro area Denmark

Sweden Switzerland

Japan Hungar

y

Bulgaria

Source: Haver Analytics. Note: the x-axis shows monthly intervals.

19

While there is some direct cost pressure coming from the charge on excess reserves, it is

dominated by the indirect cost of negative rates coming from the possible decline of net interest

income in cases where sticky deposits compress lending margins. However, bank profitability

has not worsened because positive effects have so far outweighed these adverse effects. Many

euro area banks have been able to more than offset declining interest revenues with higher

lending volumes, lower interest expenses, lower risk provisioning and capital gains (Cœuré,

2016a).

26

While bank profitability has been a longstanding structural challenge for many euro

area countries (Albertazzi and Gambacorta, 2009), the aggregate NIM has even improved

slightly towards the end of 2015, after almost 1.5 years of negative rates.

27

Moreover, reduced

lending margins have also put pressure on banks to consolidate and strengthen operational

efficiency.

28

Some banks―such as those in Sweden, Denmark and Switzerland

29

—have been

able to maintain overall profitability and benefitted from historically low impairment charges

and greater wholesale funding at negative rates (Appendix I, Box A2 and Figure 2).

26

ECB staff estimate that negative rates have contributed about one percentage point to corporate lending growth since July

2014 (Rostagno and others, 2016).

27

See Demirguc-Kunt and Huizinga (1999) for early evidence on determinants of bank interest margin and profitability from

international experience.

28

For instance, the pressure on profitability in Italy and Spain may explain why some banks have already announced significant

cuts in operating costs (closing of branches and reduction in staffing). See also Jobst and Weber (2016).

29

Also house prices have risen significantly since interest rates turned negative as the demand for mortgage loans has increased;

in this context, banks also generate more fee income from higher re-financing of mortgages.

20

Figure 3. Currency in Circulation and Pervasiveness of Negative Interest Rates

(2012-2016, percent)

IV. ASSESSMENT FOR THE EURO AREA

So far, negative interest rates have contributed to an improvement in overall financial conditions

and a modest expansion of credit. The negative deposit facility rate has been effectively

transmitted through the domestic credit channel. According to the ECB’s Bank Lending Survey

(ECB, 2016a) negative rates seem to have led to an increase in household lending in the euro

area (Figure 4 and Appendix III, Figure A4), and the impact is expected to continue going

1

2

3

4

5

6

7

8

9

10

-3 -2 -1 0 1

since July 2014

until June 2014

Negativity of Yield Curve 1/

Currency in Circulation

(y/y change)

Euro Area

0

1

2

3

4

5

6

7

-6 -4 -2 0 2

since July 2014

until June 2014

Negativity of Yield Curve 1/

Currency in Circulation

(y/y change)

Denmark

-20

-15

-10

-5

0

-2-10123

since July 2014

until June 2014

Negativity of Yield Curve 1/

Currency in Circulation

(y/y change)

Sweden

Source: Bloomberg L.P. and IMF staff calculations. Note: 1/ denotes the extent to which the 1-month interbank offer rate forward

curve is in negative territory, calculated as the product of the maturity term and the interest rate.

-5

0

5

10

15

20

25

30

-4 -3 -2 -1 0 1

since July 2014

until June 2014

Negativity of Yield Curve 1/

Currency in Circulation

(y/y change)

Switzerland

21

forward.

30

With money market rates tracking the deposit rate in an environment of excess

liquidity, the negative rate has also enhanced the ECB’s forward guidance while inflation and

inflation expectations have remained subdued. Negative rates have also strengthened portfolio

rebalancing (Heider and others, 2016)—an important transmission channel of the ECB’s asset

purchase program.

The impact of NIRP on bank profitability so far has been limited but monetary transmission

might become less effective as interest rates become more negative. Given that the volume of

outstanding loans in the euro area matches the amount of deposits, the pass-through of policy

rates to lending and deposit rates matters

greatly for the earnings capacity of most

banks. Estimates of the impact of the

recent decline in policy rates on banks’

NIMs suggest a small effect (7 basis

points for a 50-basis point reduction in the

policy rate).

31

Since the adoption of NIRP,

however, monetary transmission has

become more heterogeneous across the

euro area, especially for household

lending, with a higher pass-through in

countries with a higher share of variable

rate loans. While the extent to which

deposit rates are sticky at the ZLB remains

to be seen, lending rates would likely

decline more than deposit rates in the near term if cash demand is highly elastic (see text figure

and Rognlie, 2015). This would leave little room for further substantial adjustments to the

deposit rate without compromising banks’ net interest earnings. On the other hand, banks might

also be reluctant to reduce lending rates unless they can offset lower interest margins by

substituting wholesale funding for more expensive deposit funding, which represents a large part

30

Negative interest rates have had little impact on corporate lending volumes over the past six months, but some positive impact

is expected for the coming months.

31

NIMs have been estimated for all large euro area banks that are directly supervised by the ECB using publicly reported data

on consolidated bank balance sheets. For some banks with sizeable and, in most cases, more profitable, foreign operations, the

reported NIMs might overstate the profitability of lending within the euro area.

-0.4

-0.3

-0.2

-0.1

0

0.1

0.2

one-month response three-month response

Euro Area: Estimated Change of the

Lending Spread to a Reduction in

Effective Policy Rate, 2006-2016

(multiple) 1/

ITA

ESP

EA

FRA

DEU

Sources: Bloomberg L.P., Haver, and IMF staff calculations. Note: estimates

based on the cumulativeresponse of the lending spread (lending rate minus

deposit rate) to a one-percent reduction in the overnight money market rate

(EONIA) using a VAR specification with a simple lag structure between July

2006 and May 2016; thelending rates is the volume-weighted average

lending rate to both non-financial corporates and households.

22

of euro area bank liabilities. If lending rates become stickier, monetary transmission could

become impaired, reducing the effectiveness of negative rates as a policy measure.

Early evidence suggests that the adverse impact of negative rates on bank profitability may

increase non-linearly as the policy rate declines further.

32

Indeed, the ECB’s Bank Lending

Survey (ECB, 2016a) shows that banks’ profitability has recently declined and is expected to

remain depressed (Figure 4). Admittedly, higher aggregate demand and asset quality help raise

investment income, lower funding costs and provision expenses, which has mitigated so far the

adverse impact on bank profitability in the euro area and support the notion that the economic

lower bound to NIRP might be much lower than the ZLB (Cœuré, 2016b). However, these

benefits have weakened over time, especially in countries where the pass-through of policy rates

is high and low credit demand limit the extent to which banks (can) increase lending to offset

the impact of lower lending rates.

Deteriorating investor confidence and declining risk-taking behavior could intensify the

potentially adverse impact of negative rates. The prospect of low policy rates for a longer

time―amplified by structural challenges to banks especially in countries where the cost of risk

remains high due to a (still) large stock of impaired assets―has already worsened the outlook

for bank earnings.

33

Further substantial reductions to the deposit rate could further weigh on

banks’ equity prices as investors will be likely to revise down their expectations of banks’ future

earnings (Figure 5).

34

While monetary easing has reduced borrowing costs,

35

equity risk premia

have risen, and price-to-book ratios have declined during the second half of 2015, with the

average cost of equity now exceeding the return on equity.

36

As sustainable profitability

becomes more difficult to achieve, capital-constrained banks become more likely to reduce

lending despite declining rates.

32

Although it is unclear whether banks still have room to cut deposit rates, banks may be reluctant to do so due to competition.

33

Both level and slope of the yield curve are found to contribute positively to bank profitability in the long run (Alessandri and

Nelson, 2012; Borio and others, 2015). Busch and Memmel (2015) also find that banks’ net interest income benefits over the

medium- to long-term horizon if the interest rate level increases.

34

The return on assets for European banks is low at 0.24 percent (compared to 1.0 percent of U.S. banks).

35

For some banks the cost of borrowing might not necessarily decrease as their funding opportunities via money markets remain

limited (such as smaller banks) and/or they lengthen the maturity of their term funding.

36

This holds particularly true in countries where banks face greater earnings pressure and credit growth has been low.

23

For the euro area, three important adverse implications need to be considered in the way

negative rates could diminish the transmission of monetary policy to the real economy:

NIRP may become less effective in economies most in need of stimulus. Given the wide

deposit base in most euro area countries, the extent to which deposit rates are sticky has

a direct impact on bank profitability and the effectiveness of NIRP on monetary

transmission. Even if banks were to fund themselves increasingly via money markets,

the benefit from wholesale funding at negative rates will be limited by the existing

deposit base and cannot offset the negative impact of lower rates on existing loans if

credit growth is insufficient (Figure 3). Hence, lower profitability from financial

intermediation might override possible mitigating benefits from higher asset prices and

pricing frictions due to an insufficient reduction in funding costs. In particular, bank

profits are likely to decline in countries with large outstanding loan amounts at variable

rates if lending growth cannot offset diminishing interest margins as existing loans re-

price. In this regard, the ECB’s TLTRO II program could facilitate the transmission to

lending rates by mitigating the potentially adverse impact of negative rates on banks’

lending margins (ECB, 2016b). Higher credit demand can offset declining margins, and,

in turn, reinforce the impact of TLTRO II on bank profitability (Appendix I, Box A3).

Among countries with a high share of variable rate loans, such as Italy, Portugal, and

Spain, also high asset impairments amplify concerns about banks’ earnings capacity, and

restrict their ability to supply credit to the real economy. For instance, in the case of

Italy, NIMs have declined, and credit growth is far below the NIM-preserving threshold

(in contrast to high credit growth in Germany and France).

The direct cost of negative deposit rates is likely to be greater for banks in surplus

countries. Since the ECB charges interest only on excess liquidity the charge is greater in

those countries where banks hold large excess reserves. Given the imbalances within the

euro area, the Target 2 settlement of capital flows generates large amounts of excess

liquidity in the banking sectors of those countries with substantial current account

24

surpluses (such as Germany

and the Netherlands) vis-à-

vis other members of the

currency area.

37

In addition,

the implementation of the

Eurosystem’s asset

purchase program has

generated additional

liquidity in other core

economies in excess of their

national share of asset

purchases, such as France

(see text figure). Both

developments have led to a very uneven distribution of excess liquidity, affecting banks

differently across the euro area.

38

In principle, tiering of the deposit rate could mitigate

the direct cost of NIRP and ensure effective transmission of the marginal policy rate (to

short-term rates) even if rates became more negative and excess liquidity increases.

However, the heterogeneity of national banking systems within the euro area might

complicate the effective implementation of a tiered reserve regime (Appendix I, Box

A1).

Negative interest rates might not necessarily increase the scope of eligible assets for

purchases under the current program. Since purchases are limited to eligible

government and public agency debt securities trading at yields that are above the ECB’s

deposit facility rate, moving interest rates into deeper negative territory would make this

price-based exclusion less restrictive as more securities trading at negative yields would

become eligible for purchase. However, lowering the deposit rate will also cause yields

to fall—albeit at different degrees across the euro area depending on the yield curve

flattening—leaving some proportion of the securities trading above the lower (new)

deposit rate unchanged.

37

Note that the extent to which TLTRO II boosts the usage of ECB liquidity (and not just facilitates a rolling over of existing

liquidity), existing Target 2 imbalances are bound to increase. This would be consistent with a more positive credit impulse and

hence stronger domestic demand growth.

38

Several countries (Bulgaria, Denmark, Japan, Norway, and Switzerland) have tiered reserve systems. In the case of Japan and

Switzerland they were only introduced in conjunction with NIRP in order to reduce banks’ direct cost of holding excess reserves

(Annex, Box A1).

-100

-50

0

50

100

150

200

Germany France Italy Spain

Change of Target 2 balance (- ECB reliance)*

Change of Bank Deposits at NCB

Eurosystem purchases (PSPP) 1/

Sources: Bloomberg L.P. , ECB, Haver, NCBs, and IMF staff calculations. Note: */The use of ECB liquidity

reduces the Target 2 balance and is subtracted; 1/ public sector purchase program (PSPP).

Euro Area: Rising Financial Fragmentation, January 2015-March 2016

(absolute change, EUR billion)

25

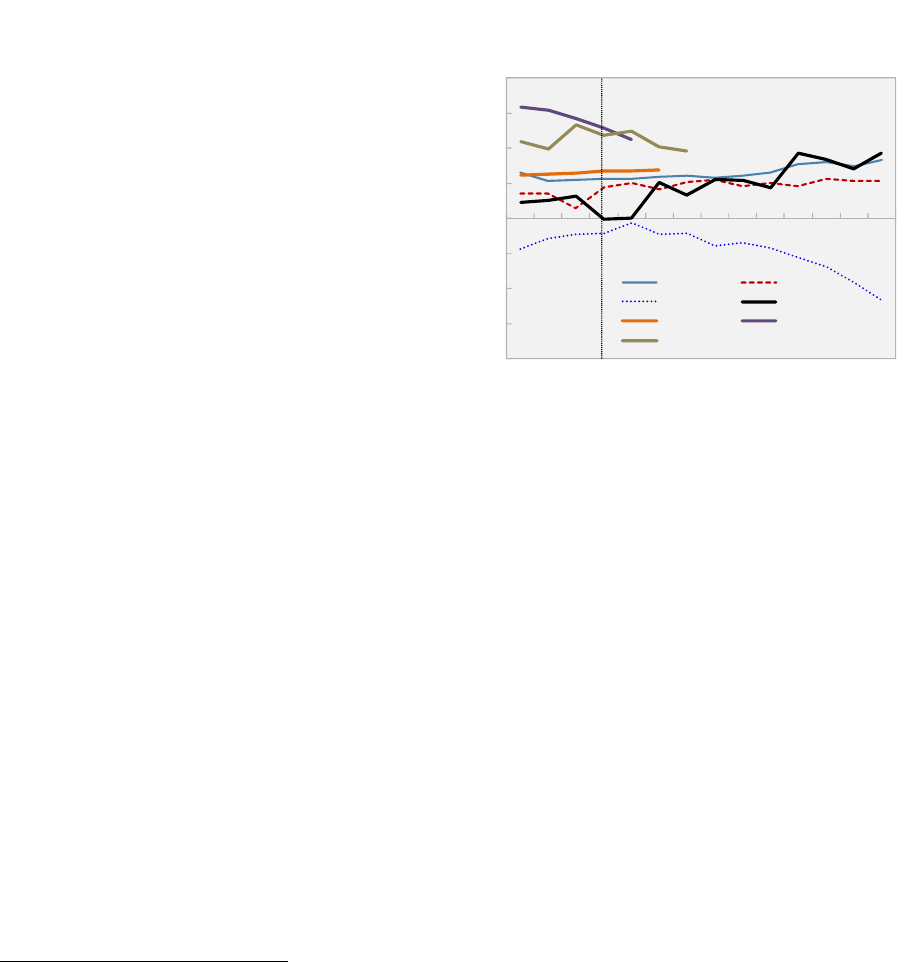

Figure 4. The Impact of NIRP on Bank Profitability and Implications for Credit Growth

Within the euro area, banks in the selected economies will likely

re-price lending quicker than deposits, reducing lending margins ...

... given the high reliance on a wide deposit base amid rising

pressure to rollover expiring term deposits.

As a result, lending margins have compressed most in countries

with high asset re-pricing and stickier deposits ...

… with higher levels of underprovisioned impaired assets weighing

on the capacity of banks to maintain their NIMs.

-0.6

-0.4

-0.2

-1E-

1

0.2

0.4

-0.6

-0.4

-0.2

1

E-15

0.2

0.4

ITA ESP EA FRA

3. Change in Lending Spread and Net Interest

Margin (NIM)

(percentage points) 1/

Lending spread (housing)

Net interest margin (total)

Sources: Bloomberg L.P., Haver, and IMF staff calculations. Notes: calculated

for new agreements between June 2014 and Jan. 2016 (lending spread) and

June 2014 and March 2016 (NIM); 1/ lending spread is calculated as the

difference between the lending rate for new business less the three-month

money market rate.

0

3

6

9

12

15

18

-0.4 -0.2 0.0 0.2 0.4

4. Change in Net Interest Margin and

Nonperforming Exposures 1/

(percent change/percent of total exposure)

Sources: Bloomberg LP, EBA Transparency Exercise (2015) and IMF staff

calculations. Note: NPEs as of end-June 2015; change of NIM between

June 2014 and March 2016.

Change in Net Interest Margin (NIM)

Stock of Nonperforming

Exposures (NPEs)

ITA

EA

ESP

FRA

DEU

Current loan growth in selected economies is insufficient to offset

the impact of declining margins ...

... and recent history suggests that it is unlikely that credit will pick

up under these conditions.

-2

-1

0

1

2

3

4

5

6

7

-2

-1

0

1

2

3

4

5

6

7

ITA ESP EA FRA DEU

5. Annual Loan Growth Required to Maintain

Net Interest Margin, end-2015

(y/y percent change) 1/

Required loan growth

Current loan growth (y/y, March 2016) 2/

Sources: Bloomberg L.P., EBA Transparency Exercise (2015), ECB, SNL, and IMF staff

cal cu lat ions. Note : 1/ b ased on th e hist orical pa ss-thr ough o f policy rate s an d the

elasticity of net interest margins to changes in term premia between Jan. 2010 and

Feb. 2016; total mortgage and corporate loans at end-2015 to EA residents.; scenario

assumes an increase of monthly asset purchases (until Sept. 2017) by the ECB and a

reduction of the deposit rate by 10bps (as per ECB decision on March 10).

ITA

ESP

EA

FRA

DEU

20

30

40

50

60

0.51.01.52.02.5

Household and corporate deposits

(percent of total liabilities)

Average interest rate on outstanding term deposits 2/

Sources: Bloomberg L.P., Haver, and IMF staff calculations. Note: 1/

MFI=monetary financial institutions; 2/ oth household and non-financial

corporates.

2. Non-MFI Deposits as a Share of Total

Liabilities and Interest Rates on Deposits, January

2016 1/

(percent)

1.15

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

-4

-3

-2

-1

0

1

2

3

4

2011 2012 2013 2014 2015 2016

Loan Growth (y/y) - Households

Loan Growth (y/y) - NFC

Net Interest Margin (rhs)

6. Euro Area: Average Net Interest Margin and

Credit Growth

(weighted by bank assets)

Sources: Bloomberg, L.P.; ECB; and IMF staff calculations.

0

0.1

0.2

0.3

0.4

0.5

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

ITA ESP EA FRA DEU

1. Estimated Sensitivity of the Average Rate of

the Loan Book and Deposit Rates to a Change

in Effective Policy Rate, 2006-2016

(multiple) 1/

Existing loans ("back book")

Deposits

Sources: Bloomberg L.P., Haver, and IMF staff calculations. Notes: based on

the cumulative response over three months to a one-percent reduction in

the overnight money market rate (EONIA) using a VAR specification with a

simple lag structure between July 2006 and May 2016; 1/ volume-weighted

average based on lending to both non-financial corporates and households.

26

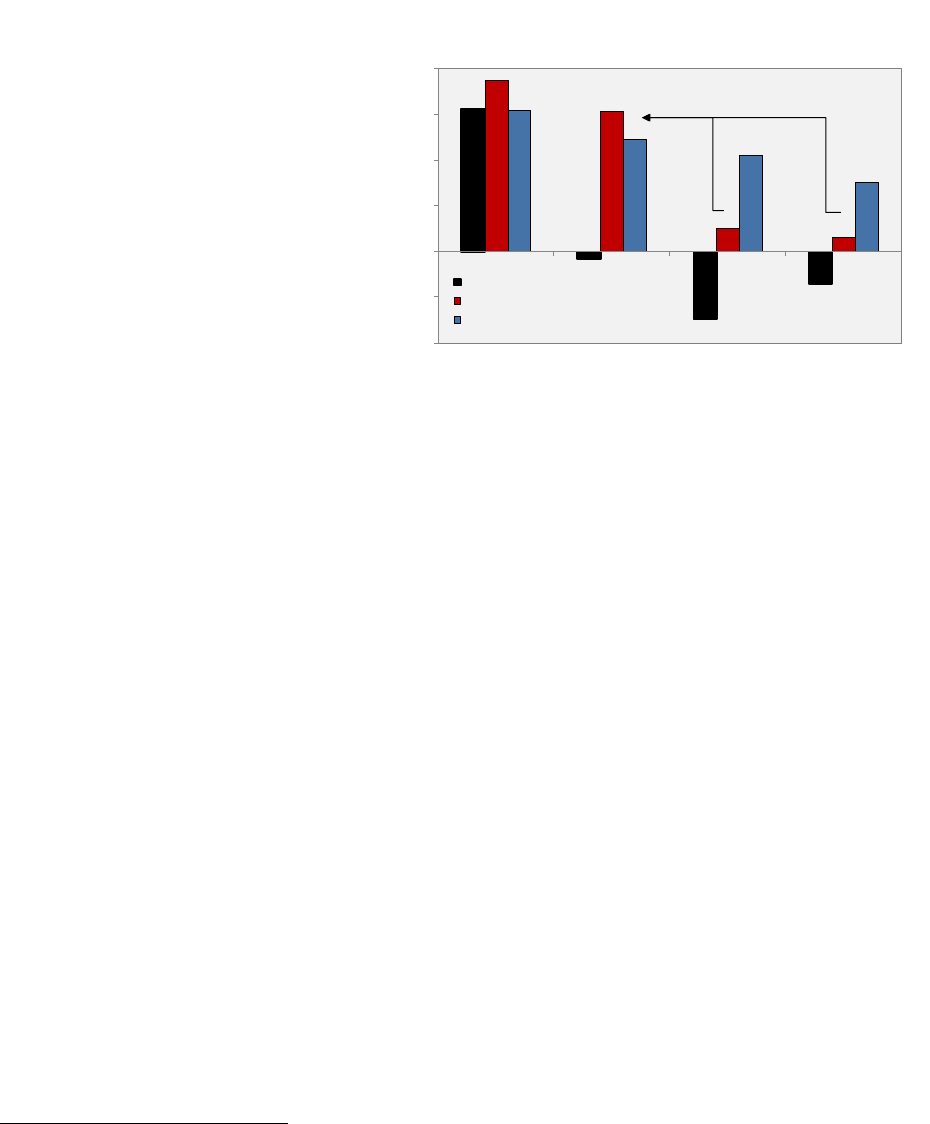

Figure 5. Bank Equity Valuation and Credit Growth

EA

AT

DE

ES

FR

GR

IT

NL

PT

-35

-30

-25

-20

-15

-10

-5

0

5

0.51.01.52.02.53.0

Change in equity price

Avg. net interest margin

Banking Sector: Change in Equity Price and

Net Interest Margin, since 2015

(percent) 1/

Sources: Bloomberg, L.P.; and IMF staff calculations. Note: 1/ Change in equity

price and average net interest margin (NIM) between April 2015 and March

2016.

0.4

0.5

0.6

0.7

0.8

0.9

1.0

-5

-4

-3

-2

-1

0

1

2

3

4

5

2010 2011 2012 2013 2014 2015 2016

Loan Growth (y/y)

Price-to-Book Ratio

Euro Area Banks: Price-to-Book Ratio and Credit

Growth

(weighted by bank assets)

Sources: Bloomberg, L.P.; and IMF staff calculations.

EA

AT

BE

DE

ES

FI

FR

GR

IT

NL

PT

0.0

0.5

1.0

1.5

2.0

-6-4-202468

Avg. price-to-book ratio

Avg. monthly credit growth

Banking Sector: Price-to-Book Ratio and

Credit Growth, since 2015

(percent) 1/

Sources: Bloomberg, L.P.; and IMF staff calculations. Note: 1/ Cha nge i n price-to-

book va lue a nd credit gro wth between April 2015 a nd Ma rch 2016.

-1

0

1

2

3

4

5

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016

Euro Area: Bank Equity Prices, Inflation

Expectations, and Sovereign Yields

(Index 2010 = Jan. 2010/Percent)

Euro Area bank equity (lhs)

Euro Area 1y inflation expectations (rhs)

Euro area 10y sovereign yields (rhs)

Source: Bloomberg, LP.

-1

0

1

2

3

4

5

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016

United States: Bank Equity Prices, Inflation

Expectations, and Sovereign Yields

(Index 2010 = Jan. 2010/Percent)

US bank equity (lhs)

US 1y inflation expectations (rhs)

US 10y sovereign yields (rhs)

Source: Bloomberg, LP.

Banks with weaker profitability experienced a larger decline in

equity prices since 2015 ...

... with low equity valuations raising the cost of equity.

The impact of lower returns on valuations has made banks less

willing to lend ...

... with credit supply lagging a recovery in bank equity.

The combined effect of low inflation and low expected profitability

has depressed equity valuations of euro area banks ...

... while U.S. banks have benefitted strongly from monetary easing,

falling only recently as a result a broader market deterioration.

80

85

90

95

100

105

110

115

120

125

Jan-15 Apr-15 Jul-15 Oct-15 Jan-16 Apr-16

Equity Risk Premium

(index, Jan. 2015 = 100)

Euro Area

Germany

France

Italy

start of PSPP

Sources: Bloomberg, L.P.; and IMF staff calculations.

27

V. CONCLUSION

Negative interest rates so far have had a positive effect on the economy, helping to lower bank

funding costs and boost asset prices. In addition, negative rates have significantly enhanced the

signaling effect of the ECB’s monetary stance strengthening its forward guidance. Lowering the

deposit rate has also supported the portfolio rebalancing channel of the ECB’s asset purchase

program by encouraging banks to substitute investment in riskier assets

for excess reserves.

With money market rates tracking the

deposit rate in an environment of excess

liquidity, this has enhanced the ECB’s

signaling capacity and strengthened its

commitment to keep rates low for an

extended period of time until the price

stability objective is achieved. In some

countries, rate cuts have been passed

through to corporate and household

borrowers thereby contributing to a modest

credit expansion and bolstering the

economic recovery. Lower lending rates

have encouraged higher credit demand as

lending standards continue to ease.

Concerns about their negative effect on bank

profitability have for the most part not yet materialized.

However, further substantial reductions of the deposit rate will likely entail diminishing returns,

since the lending channel is crucially influenced by banks’ expected profitability. While most

banks have been able to mitigate the squeeze on profitability with higher lending volumes and

benefitted from higher asset prices, lower funding costs, and possible cost savings from greater

operational efficiency and consolidation, there are clearly limits to such mitigation measures.

The outlook for bank profitability has worsened recently. This is particularly relevant in euro

area countries with a high share of variable rate loans (and a high dependence on deposit

funding), where concerns about sustainable bank profitability are amplified by low credit

growth. Additional rate cuts could weaken monetary transmission if lending rates fail to adjust

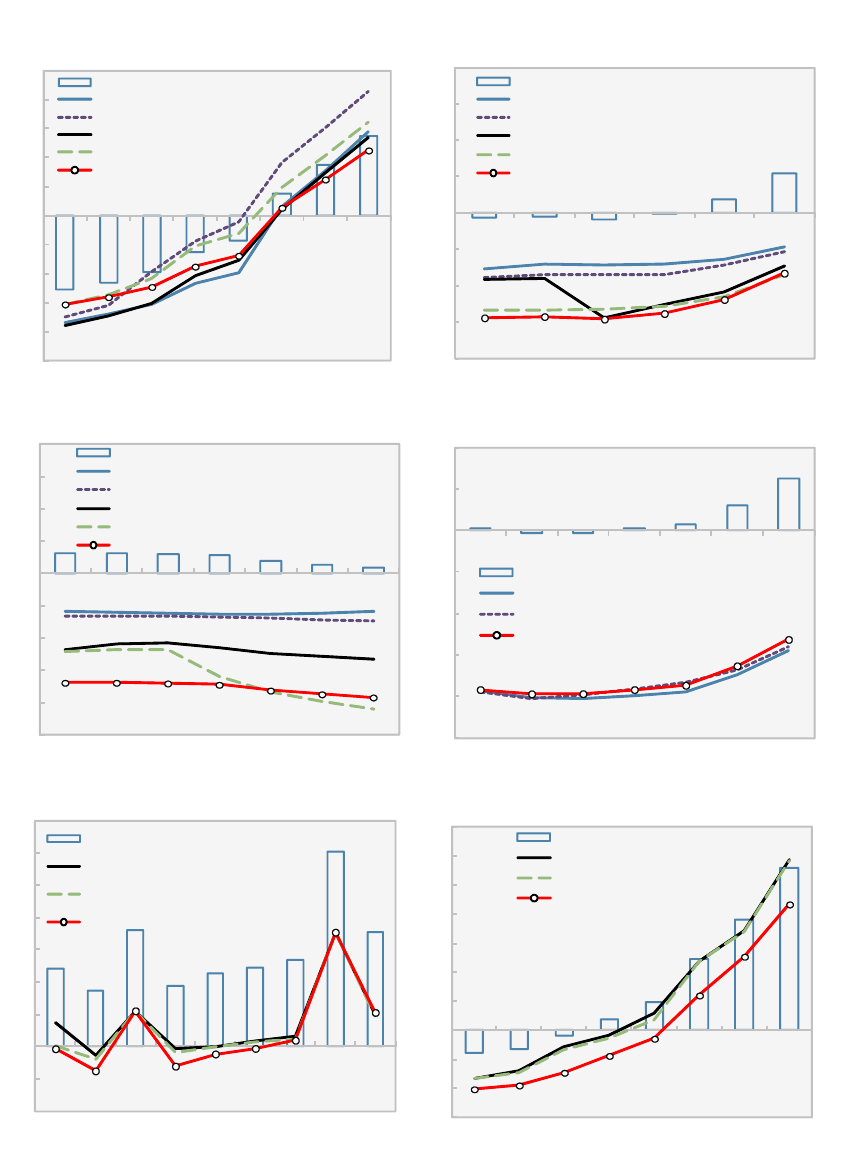

0

2

4

6

8

2011 2012 2013 2014 2015 2016

Euro area

Japan

Switzerland

Equivalency of Government Bond Yield and

Marginal Policy Rate

(Years) 1/

Source: Bloomberg LP and IMF staff calculations. Note: Euro area

covers the core economies only; 1/ the "equivalency line" shows